-01%201.svg)

Key takeaways

- TDS vs TCS, in one line: TDS means the payer deducts tax on payments like contractors or professional fees, TCS means the seller collects tax on specified receipts like high-value goods sales.

- Interplay 194Q vs 206C(1H): no double levy, whichever obligation triggers first applies, as clarified by CBDT Circular 17/2021.

- Deadlines matter: monthly deposits by the 7th, quarterly statements soon after the quarter, delays attract ₹200/day fee and 1-1.5% monthly interest.

- Tally Prime readiness: enable TDS/TCS, map Nature of Payment, capture PANs, and track thresholds per party.

- Thresholds to remember: 194Q at ₹50 lakh per seller for goods purchases, 206C(1H) at ₹50 lakh per buyer for goods sales, special 206C(1G) rules for foreign remittances.

TCS vs TDS, the short answer

Month-end decisions get easier when you know who acts. TDS is where the payer deducts tax at source on specified payments, while TCS is where the seller collects tax from the buyer on specified receipts. Both need monthly deposits and quarterly returns, both carry interest and fees if delayed.

Common TDS sections: 194C for contractors at 1-2%, 194H for commission at 5%, 194J for professional fees at 10%, 194Q for purchase of goods at 0.1%. For rules and forms, see ITD Portal TDS Compliance.

Common TCS sections: 206C(1H) for sale of goods receipts exceeding ₹50 lakh per buyer at 0.1%, 206C(1G) for certain foreign remittances at 0.5-20%. Reference: Income Tax Act Section 206C.

In practice: TDS sits on the AP side of your books, TCS sits on the AR side. Set up both workflows to avoid last-minute penalties.

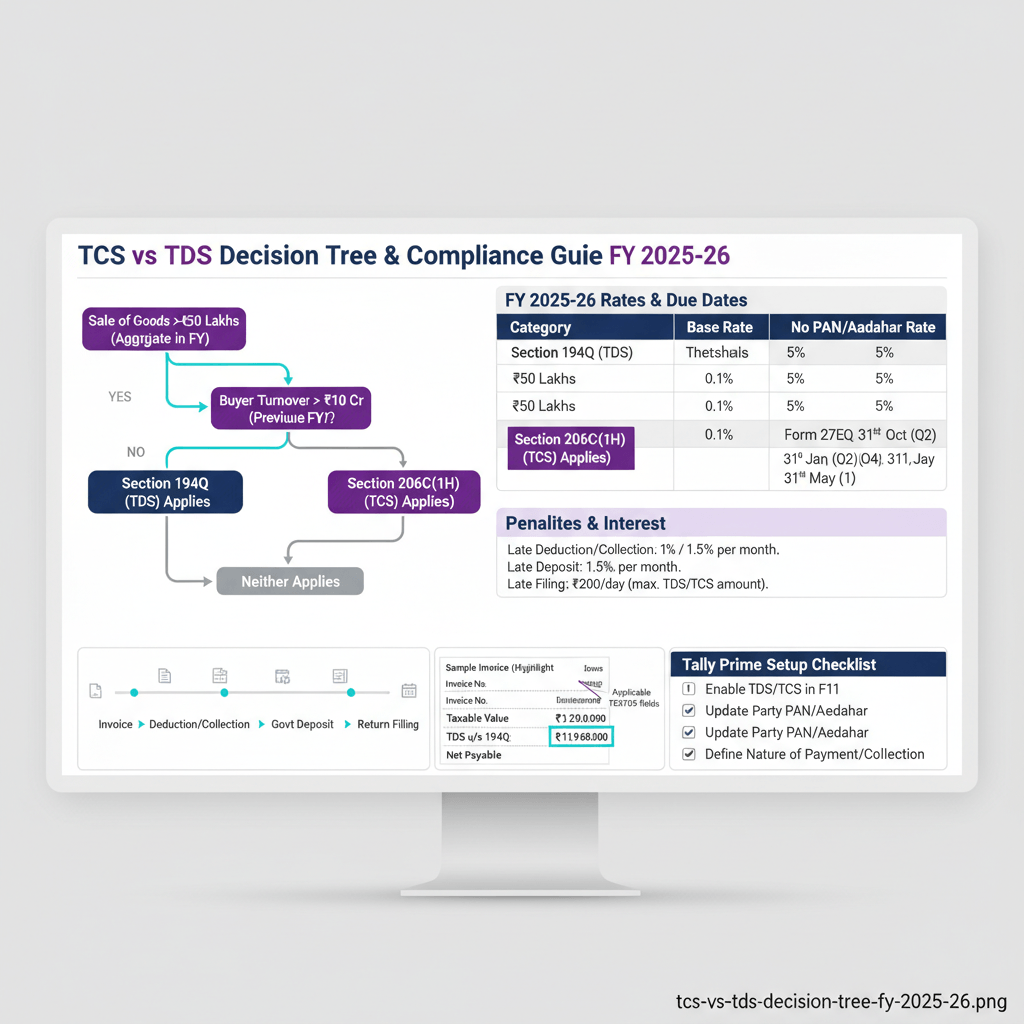

The decision tree to choose TDS or TCS

Use this stepwise logic for every invoice, payment, or receipt.

- Is it your payment (AP)? Evaluate sections like 194C, 194H, 194J, or 194Q, and deduct TDS if thresholds apply.

- Is it your receipt (AR)? Evaluate TCS sections like 206C(1H) or 206C(1G), collect TCS when thresholds are crossed.

- E-commerce operator angle? If an operator facilitates the sale, Section 194-O at 1% applies on gross, see ITD Section 194-O.

- Goods purchase vs sale (194Q vs 206C(1H)): Only one applies—whichever event occurs first governs, clarified by CBDT Circular 17/2021. Exclude GST from threshold if shown separately.

- PAN/Aadhaar not furnished? Apply higher rates, up to 20% for non-filers or 5% for 206C(1H) without PAN.

- Track party-wise FY thresholds: Reset on 1 April, maintain running totals per vendor and per customer.

Manual tracking is tedious and error-prone. AI Accountant’s AP and bill automation reads invoices, validates PANs, predicts applicable sections like 194Q or 206C(1H), and syncs Tally-ready entries.

Rates and thresholds at a glance

Popular TDS sections:

- 194C: contractors/sub-contractors, 1% for individuals/HUFs, 2% otherwise, thresholds apply.

- 194H: commission or brokerage, 5%.

- 194J: professional or technical fees, 10%.

- 194Q: purchase of goods, 0.1% on amounts exceeding ₹50 lakh per seller.

Popular TCS sections:

- 206C(1H): sale of goods, 0.1% on receipts exceeding ₹50 lakh per buyer in a year.

- 206C(1G): foreign remittances under LRS, 0.5-20% depending on purpose and threshold, per Notification 30/2023.

Real-world scenarios to apply the rules

AP side examples

- Contractor bill of ₹5,00,000 (194C): If the annual threshold is crossed, deduct 1% or 2% depending on payee type.

- Professional fees of ₹2,00,000 (194J): Deduct 10% TDS, typically without an annual threshold.

- Goods purchase of ₹60,00,000 from a vendor (194Q): Deduct 0.1% on ₹10,00,000 exceeding ₹50 lakh, assuming other conditions met and GST shown separately is excluded.

AR side examples

- Goods sale where cumulative receipts reach ₹55,00,000 (206C(1H)): Collect 0.1% on ₹5,00,000, on receipt basis including advances, as guided by CBDT Circular 17/2021.

- Sales return in next period: Adjust excess TCS in subsequent receipts from the same buyer.

Marketplaces and operators

If you sell through an operator, 1% under 194-O is deducted on gross receipts by the operator, typically overriding 194Q or 206C(1H) for the same flow.

Foreign remittance overview under 206C(1G)

- Education financed by a loan: 0.5% above ₹7 lakh.

- Education or medical without a loan: 5% above ₹7 lakh.

- Other purposes: 20% above ₹7 lakh.

- Overseas tour packages: 20%, no threshold. See Notification 30/2023 for specifics.

Edge cases to watch

- No PAN provided: Higher TCS rate, for instance 5% under 206C(1H).

- Credit notes and rate changes: Adjust collection in the next cycle per ITD FAQs.

Compliance calendar, interest, and penalties

Deposits: For April to February, deposit by the 7th of the next month, for March TDS deposit by 30 April, TCS by 7 April.

Quarterly returns: TDS—31 July, 31 October, 31 January, 31 May. TCS—15 July, 15 October, 15 January, 15 May.

Interest and fees:

- TDS non-deduction: 1% per month.

- TDS deducted but paid late: 1.5% per month.

- TCS failure: 1% per month.

- Late filing fee: ₹200/day under 234E, plus penalty between ₹10,000 and ₹1,00,000 under 271H.

See ITD TDS Compliance and relevant sections for detailed computation. For common errors that trigger notices, review this guide on TDS mistakes and income tax notices.

Tip: Use challan CRN and BSR codes to reconcile quickly against books and 26AS/AIS—avoid month-end surprises.

Accounting entries and Tally Prime setup

Tally Prime configuration checklist:

- Enable TDS/TCS at Gateway of Tally > F11 > Statutory & Taxation.

- Create Nature of Payment masters, for example “194J Professional Fees” at 10%.

- Capture party PANs, link the appropriate Nature of Payment, set thresholds.

- Test auto-calculation on sample vouchers. Reference: Tally TDS Setup Guide.

Entry illustration, 194J on a ₹1,00,000 invoice:

- Dr Professional Fees Expense ₹90,000

- Dr TDS Payable (194J) ₹10,000

- Cr Vendor Payable ₹1,00,000

TCS receipt under 206C(1H): On receipts after the ₹50 lakh threshold per buyer, Tally computes 0.1% automatically when configured.

Challan reconciliation: Match ITNS 281 challans via CRN and BSR codes from NSDL e-Pay Tax, then confirm in AIS at the ITD Portal. AI Accountant’s bank statement ingestion identifies tax challans and suggests ledger postings for 1-click reconciliation.

Month-end and quarter-end SOP

Weekly: Review threshold breach reports, update missing PANs, and watch upcoming TDS/TCS obligations.

Monthly by the 5th:

- AP: Run vendor-wise TDS liability, validate calculations, deposit by the 7th.

- AR: Summarise receipts for TCS, track per-buyer accumulations, deposit by the 7th.

- Bank: Download e-Pay Tax receipts, match CRN/BSR to books, post challans.

Quarterly before filing: Reconcile books against 26AS/AIS, fix mismatches, file TDS by month-end and TCS by mid-month post-quarter.

Scaling across entities: Standardise Nature of Payment, maintain consolidated threshold trackers, and centralise PAN validations. AI Accountant’s multi-org support helps CAs manage thresholds, challans, and filings across dozens of client entities from one login.

Conclusion

Implement this playbook now: apply the decision tree every time, configure Tally once and reuse, and follow the calendar rigorously. When in doubt, revisit ITD TDS Compliance and CBDT circulars.

Related reading: GSTR-2B reconciliation best practices, Section 194Q TDS on purchase of goods, Tally automation for CAs and SMEs.

FAQ

What is the core difference between TDS and TCS, and who books it in accounts?

TDS is deducted by the payer on specified payments like contractors, professional fees, and goods purchases under sections 192-194 and 194Q, while TCS is collected by the seller on specified receipts like goods sale receipts under 206C(1H). AP teams normally handle TDS, AR teams handle TCS. For legal references, see Income Tax Act Sections 192-194 and 206C. AI Accountant can auto-route entries to the right ledgers and modules.

Under 194Q vs 206C(1H), who has the primary obligation, buyer or seller, and when does no double levy apply?

Only one provision operates—whichever triggers first based on event sequence. If buyer crosses the purchase threshold first, 194Q applies and the seller need not collect 206C(1H). If seller collects first on receipt, 206C(1H) applies and the buyer does not deduct 194Q on that portion. Refer to CBDT Circular 17/2021. AI Accountant flags the first applicable trigger and tags the invoice accordingly.

How do CAs compute TDS under 194Q when GST is shown separately on the invoice?

When GST is indicated separately, it is generally excluded from the value for TDS under 194Q per CBDT guidance. Compute 0.1% on the value exceeding ₹50 lakh per seller, net of separately shown GST. AI Accountant extracts tax components from invoices and computes the net base automatically.

What are the exact due dates for TDS and TCS deposits and quarterly returns for FY 2025-26?

Deposits are due by the 7th of the following month for April to February, for March TDS by 30 April and TCS by 7 April. TDS returns are due on 31 July, 31 October, 31 January, and 31 May, TCS returns on 15 July, 15 October, 15 January, and 15 May. See ITD TDS Compliance for current forms and timelines. AI Accountant generates deposit checklists and filing calendars.

What are the interest and penalty mechanics for late deduction, late deposit, and late filing?

For TDS non-deduction, interest is 1% per month, for TDS deducted but deposited late, interest is 1.5% per month. For TCS failures, interest is 1% per month. Late filing fee is ₹200 per day under 234E, and penalty under 271H ranges from ₹10,000 to ₹1,00,000. Statutory references: Sections 201(1A), 206C(7), 234E, 271H. AI Accountant alerts you before accruals start.

How should entries be posted in Tally Prime for a 194J invoice and its payment?

At booking: Dr Expense ₹90,000, Dr TDS Payable ₹10,000, Cr Vendor ₹1,00,000. At payment: Dr Vendor ₹1,00,000, Cr Bank ₹90,000, Cr TDS Payable ₹10,000. Configure Tally as per the Tally TDS Setup Guide. AI Accountant posts voucher-ready data to Tally with correct ledgers and natures.

How does 206C(1G) TCS on LRS remittances work after 1 October 2023, and how should clients plan cash flows?

Education financed by a loan attracts 0.5% above ₹7 lakh, education or medical without a loan attracts 5% above ₹7 lakh, other purposes attract 20% above ₹7 lakh, and overseas tour packages attract 20% with no threshold. See Notification 30/2023. AI Accountant aggregates per-PAN remittances to predict when thresholds will be breached.

What documentation is needed for reconciling challans with 26AS/AIS, and how can this be automated?

Keep CRN, BSR code, date, amount, and challan serial number from NSDL e-Pay Tax. Reconcile against AIS/26AS in the ITD Portal. AI Accountant’s bank statement ingestion picks up CRN/BSR from narrations and auto-matches to books and AIS.

For marketplace sales via an operator, should clients apply 194Q or 206C(1H) in addition to 194-O?

Section 194-O obligates the e-commerce operator to deduct 1% on gross; generally, buyers and sellers do not apply 194Q or 206C(1H) on the same flow. Still, review contractual flows for ancillary charges. AI Accountant tags marketplace transactions and suppresses duplicate levies.

How to treat advances, credit notes, and sales returns for 206C(1H) calculations?

206C(1H) operates on a receipt basis and includes advances; for credit notes or returns, adjust TCS in subsequent receipts from the same buyer as per CBDT FAQs. AI Accountant maintains a buyer-wise running ledger to net such adjustments and recompute TCS due.

If a vendor or customer does not share PAN/Aadhaar, what rates apply and how should books reflect this?

Higher rates apply; for example, 5% TCS under 206C(1H) without PAN, or up to 20% for certain non-filer cases. Create separate Nature of Payment or collection configurations to capture higher-rate liabilities and disclosure. AI Accountant auto-applies higher rates when PAN is missing and logs exceptions for follow-up.

Can AI tools really reduce month-end TDS/TCS errors for CA firms, and what is a practical setup?

Yes, by automating invoice capture, PAN validation, section prediction, and threshold tracking across entities. A practical setup is to use AI Accountant for ingestion and computation, then push vouchers to Tally, reconcile challans from bank feeds, and finally validate against AIS/26AS before filing. This typically reduces processing time by 50-70% and error rates to under 1% based on CA firm benchmarks.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.