Key takeaways

- Non-PO invoices are vendor bills raised without an accompanying purchase order, common in India for rent, utilities, subscriptions, professional fees, reimbursements, and one-off urgent buys.

- Compliance remains identical to PO bills, ensure valid GST invoice, e-invoice IRN where applicable, correct RCM treatment, and timely TDS deduction and deposit.

- A clear policy with monetary thresholds, category rules, documentation requirements, and an approval matrix keeps speed and control in balance.

- A practical SOP covers intake, validation, accounting, tax computation, approvals, payment, and month-end reconciliation, with maker-checker controls.

- Tally Prime and Zoho Books both handle non-PO bills effectively, including ITC, TDS, RCM, advances, duplicates, and month-end checks.

- Strong controls without POs include two-way matching to contracts or approvals, duplicate detection using hashes, and monthly vendor reconciliations.

- Automation becomes essential beyond moderate volume, AI Accountant integrates with Tally and Zoho Books, automates extraction, validation, and GSTR-2B reconciliation.

- Measure cycle time, exception rate, ITC and TDS compliance, cost per invoice, and vendor data quality to drive continuous improvement.

What exactly is a non-PO invoice?

A non-PO invoice is any vendor bill that arrives without a pre-approved purchase order backing it. In practice, these cover everyday spend that keeps the business running, for example rent, utilities, SaaS subscriptions, legal and consulting fees, emergency repairs, team travel, and reimbursements. The classic three-way match gives way to a simpler process, you typically have the invoice plus supporting documents like email approvals, contracts, or delivery proofs.

Speed improves, yet control gaps appear, the risk is duplicate payments, incorrect tax, fake vendors, or misclassified expenses. That is why the approval trail, documentation, and reconciliations matter even more for non-PO invoices. For a primer with examples, see non-PO invoice guides and comparisons like PO and non-PO invoice and PO, non-PO difference.

Golden rule: absence of a PO never reduces your compliance or documentation burden, it simply shifts where controls must operate.

Understanding compliance requirements for non-PO bills

GST and TDS obligations apply irrespective of a PO. For GST Input Tax Credit, ensure a valid tax invoice, proof of receipt of goods or services, and GSTR-2B match. Capture e-invoice IRN and QR where applicable. For scenarios like GTA, legal services, or imports, apply Reverse Charge Mechanism correctly, then claim ITC in the eligible period.

TDS requires correct section, rate, and timing, for example 194C for contracts, 194J for professional services, 194I for rent, 194H for commission. Deduct at the earlier of credit or payment, include advances, and deposit within timelines. Without a PO audit trail, shore up controls through maker-checker, documented approvals, vendor KYC with GSTIN validation, and tight reconciliation. Background reading: PO and non-PO invoice, and control expectations discussed in PO vs non-PO explained.

Creating your non-PO invoice policy framework

Define what qualifies for non-PO processing and what must go through procurement. Set clear thresholds, for example genuine ad-hoc spends under ₹25,000 can be non-PO, planned purchases and all goods deliveries must use POs. Build an approval matrix by amount and category, for example under ₹10,000, department head, over ₹50,000, finance controller, legal fees or statutory dues, special routing regardless of amount.

Mandate documents, invoice, approval evidence, proof of delivery or service completion, vendor KYC with verified GSTIN and bank details, IRN for e-invoices. Define tax rules category wise, ITC eligibility, TDS section and exception handling. Set SLAs, for example 48 hours for regular bills, 24 hours for statutory payments. Work back from compliance deadlines, submission on the 14th, processing by the 17th, GSTR due on the 20th.

Tip: Make two-way matching to contracts, SOWs, or email approvals a hard gate before payment, this compensates for the missing PO.

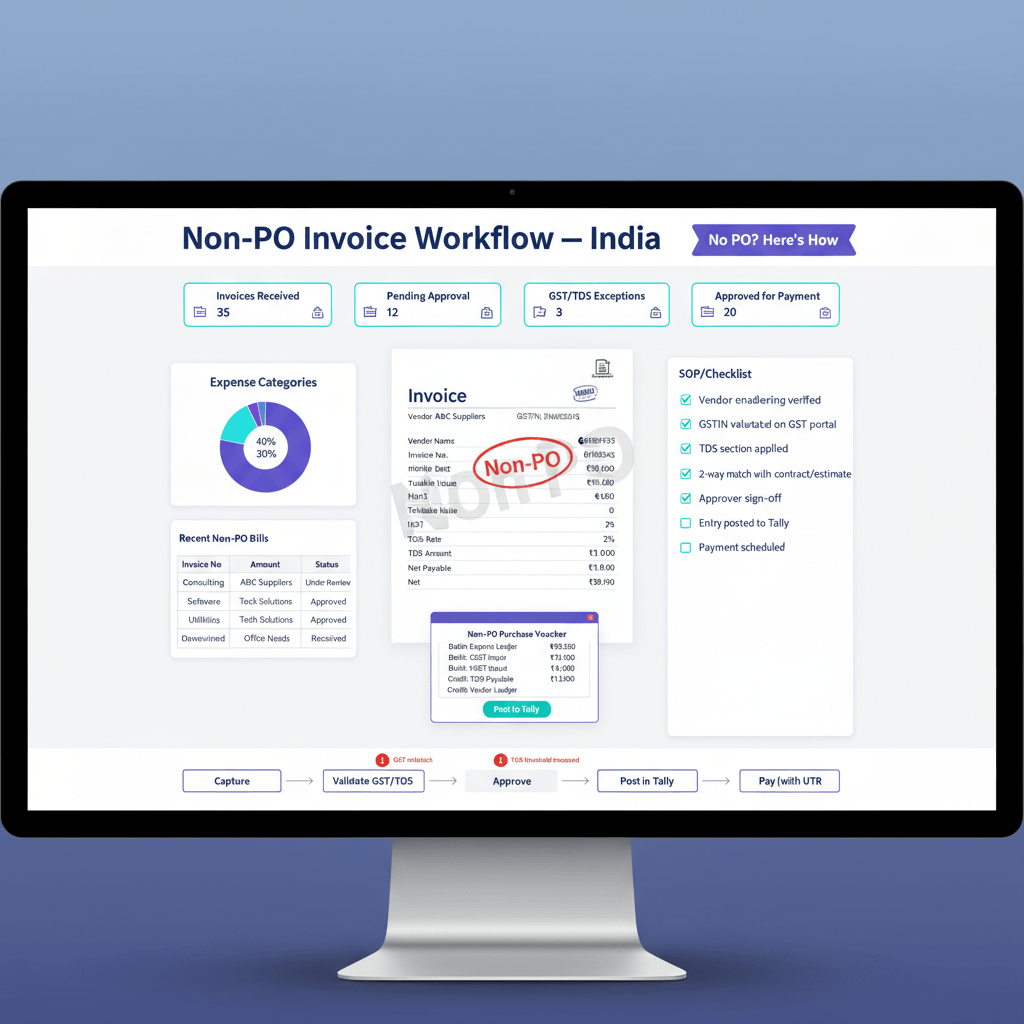

Step-by-step SOP for processing non-PO invoices

Step 1: Invoice intake

Centralize all channels, email, shared drive, or a vendor portal. Scan physical bills immediately, name files consistently, vendor code, invoice number, date.

Step 2: Initial validation

Verify vendor master details, exact GSTIN match, legal name, address. Check duplicate invoice numbers for the same vendor, verify arithmetic and tax breakup, evaluate place of supply and RCM applicability.

Step 3: Accounting classification

Decide expense or capitalization, assign GLs, cost centers, and projects. Handle advances and adjustments carefully to avoid misstated outstanding balances.

Step 4: Tax computation

Apply correct GST based on supply type, compute TDS under the right section, flag RCM liabilities for separate booking and later ITC claim.

Step 5: Approval routing

Route per matrix, maintain audit trails showing who approved and when. Escalate delays automatically, capture comments inline for context.

Step 6: Payment processing

Link bills to payments, support partials and retentions, reconcile advances, ensure TDS deposit timelines are met.

Step 7: Month-end activities

Match purchase register to GSTR-2B, book accruals for unbilled services, put risky vendor ITC on hold, run duplicate and exception reports.

Non-PO bill processing in Tally Prime: practical guide

Initial configuration

Enable GST and bill-wise details in F11. Configure purchase vouchers in accounting mode. Create supplier ledgers with GSTIN and terms, expense ledgers mapped to the right groups, and TDS ledgers under applicable sections.

Recording a vendor bill without PO

Open a Purchase voucher, pick supplier ledger, enter invoice number and date as bill reference, add expense ledgers, GST auto-calculates if configured, set due date from terms. For TDS, apply in the purchase voucher using configured ledgers, or pass a journal entry, always tag the same bill reference.

Handling RCM transactions

Use a Journal voucher, debit expense, credit RCM liability, mark the tax classification for RCM, then pass the ITC claim entry in the eligible period that aligns with returns.

Managing advances

Record advance payments with Payment voucher using an Advance tag, later link to the bill during reconciliation so Tally adjusts the outstanding automatically. For a deeper explainer on processes, see Managing Advances.

Duplicate detection and month end

Use consistent bill references, review the Duplicate Bills report and Day Book for patterns. At month end, run Outstanding Analysis, TDS Outstanding, and GST Reports, then compare GSTR-2B with the purchase register for mismatches.

Zoho Books approach for non-PO invoices

Create a Bill directly, attach digital documents, map expenses to correct accounts, GST computes as per tax settings. Toggle Reverse Charge for RCM liabilities. Apply TDS by selecting the section, Zoho computes and tracks deposits. Link partial payments and advances, surface status to vendors through the portal. Month end, reconcile with GSTR-2B, track ITC status, and fix mismatches with the built-in tools.

Implementing controls without purchase orders

Two-way matching

Match invoices to contracts or SOWs, completion certificates or delivery receipts, or documented email approvals. This becomes the control anchor.

Duplicate prevention

Create a unique hash of vendor code, invoice date, and amount, flag all matches for review. Reconcile vendor statements monthly to catch strays that evade system checks.

Risk mitigation

Validate GSTINs against public lists monthly, hold ITC for new vendors until GSTR-2B reflects the document, impose budget checks at approval, and review unusual spend patterns.

Technology enablers

Adopt OCR for data capture, digital logs for service delivery, and simple workflow tools for approvals. Practical over perfect, even a structured spreadsheet is a big upgrade from email chaos. For comparisons and ideas, see PO vs non-PO explained and touchless invoice processing.

Automation tools for non-PO invoice processing

1. AI Accountant

Purpose built for Indian businesses, it automates intake, OCR extraction, GSTIN and vendor mismatch detection, ledger prediction, and direct sync to Tally or Zoho Books. The GSTR-2B reconciliation flags ITC mismatches instantly, saving days each month.

2. QuickBooks, 3. Xero, 4. SAP Concur, 5. FreshBooks, 6. Tally with add-ons

These offer increasing levels of workflow and automation. Evaluate fit for Indian GST and TDS specifics, integration with your ledgers, and total cost of ownership. For a technology overview, see automating PO, non-PO, AP.

Recommendation: If you already run Tally or Zoho Books, AI Accountant provides the least disruptive path to automation with fast ROI.

Measuring success: key metrics to track

Cycle time

Receipt to posting, approval turnaround, invoice date to payment. Best teams process non-PO invoices inside 48 hours.

Quality and compliance

Exception rate below 5 percent, near zero duplicates, high tax accuracy, ITC match rate above 98 percent, zero TDS deposit delays.

Cost and control

Processing cost per invoice, early payment discount capture, non-PO spend as a share of total, and vendor master completeness. Clean vendor data prevents most processing issues.

Handling special cases and edge scenarios

Employee reimbursements

Treat as vendor bills tagged to the employee or pass journals with full supports. Map ITC where eligible, avoid blocked credits, apply TDS if thresholds trigger, store all approvals.

Foreign vendor invoices

Apply RCM for most imports and cross border services, use correct RBI or customs rate, complete KYC for FEMA, consider treaty withholding, and document business purpose clearly.

Credit and debit notes

Reference the original invoice, reflect GST adjustments, and true up TDS if the base changes.

Accruals and provisions

Book unbilled services at month end, reverse when invoices arrive, keep workings and approvals attached.

Petty cash

Use an imprest system with periodic true up, capture vendor details for ITC where applicable, and restrict eligible categories.

Taking action: your next steps

Draft a practical SOP with thresholds, approvals, and documents, secure buy-in, and train users. Map your current flow, find the slowest or riskiest points, and fix those first. Instrument metrics, cycle time and exception rate to start, then expand. If volume is high, consider AI Accountant to automate intake, validation, and reconciliation while syncing to Tally or Zoho Books. Small consistent improvements compound, come audit time you will appreciate the clean trails and timely compliance.

FAQ

Is a purchase order mandatory for every vendor payment in India, or can I process non-PO invoices safely?

A PO is not legally mandatory, non-PO invoices are valid. The key is robust documentation, a clear approval trail, correct GST and TDS treatment, and vendor KYC. Many SMEs and CA firms use a policy threshold, ad-hoc low value expenses can be non-PO, planned or goods related buys must use POs.

Can I claim ITC on non-PO invoices, what checks should I enforce before claiming?

Yes, ITC eligibility depends on valid GST invoice fields, receipt of goods or services, and GSTR-2B reflection. Capture e-invoice IRN where applicable, verify supplier GSTIN, and ensure the invoice appears in 2B before finalizing ITC. Tools like AI Accountant auto match purchase registers with 2B to prevent ineligible claims.

How should a CA firm configure TDS for non-PO bills in Tally Prime, including rent and professional fees?

Create TDS ledgers under the correct sections, for example 194I for rent, 194J for professional fees, enable bill wise details, and apply TDS either in the purchase voucher or through a journal entry referencing the bill. Reconcile TDS Outstanding regularly and deposit within due dates.

What is the cleanest way to handle RCM on non-PO invoices across multiple branches?

Use a standard journal entry template, debit expense, credit RCM liability, post tax wise per registration, then claim ITC via a separate journal in the eligible period. Maintain documentary evidence, contract, service completion mail, and ensure registration wise reporting aligns with returns.

How do I prevent duplicate payments without POs, is there a practical hash formula?

Use a composite key, vendor code plus invoice date plus invoice amount, optionally invoice number. Hash this key in your tracker, flag collisions for review. Run weekly duplicate scans and perform monthly vendor statement reconciliations. AI Accountant automates duplicate detection using these patterns.

Do I deduct TDS on the GST component for non-PO services, for example under section 194J?

As a practical convention, TDS applies on the amount excluding GST where GST is indicated separately on the invoice, subject to the latest CBDT clarifications and your auditor’s guidance. Configure your system to compute TDS on taxable value, then verify edge cases like composite invoices.

How should I book and later adjust vendor advances against non-PO bills in Tally and Zoho Books?

Record advances as advance entries against the vendor, not as expenses. When the invoice arrives, post the bill and link the advance during payment or reconciliation so the outstanding reduces correctly. In Zoho Books, apply the advance to the bill from the vendor credits. For repeat scenarios, AI Accountant can surface suggested linkages.

What evidence will satisfy auditors for non-PO invoices in lieu of a purchase order?

Maintain a two-way match, the invoice plus at least one strong support, such as a signed contract or SOW, email approval with scope and value, completion certificate, or delivery receipt. Keep vendor KYC, GSTIN validation, and bank verification on file. Capture approval timestamps and approver identity for maker checker.

How do I reconcile GSTR-2B with my purchase register for non-PO invoices quickly at month end?

Export the purchase register, normalize supplier GSTIN, invoice number, date, taxable value, and tax amounts, then perform a join against 2B. Investigate gaps, for example supplier not filed, number mismatch, or RCM cases. AI Accountant automates this match and tags exceptions by root cause.

Which non-PO expense categories are common ITC blocked credits I should watch out for?

Blocked credits commonly include motor vehicles in many cases, personal consumption, membership fees, certain employee related expenses, and works contract for immovable property, subject to statute and updates. Train requesters to submit correct documentation and flag blocked categories at intake.

What cycle time and exception benchmarks should a CA firm target for non-PO invoice handling?

For SMEs with moderate volume, aim for receipt to posting within 48 hours, exception rate under 5 percent, ITC match above 98 percent, zero TDS delays. Measure approver wise turnaround and address bottlenecks with a tighter matrix or automated nudges.

Can AI Accountant integrate with Tally or Zoho Books for non-PO invoices, what does the workflow look like?

Yes, AI Accountant ingests PDFs or emails, extracts key fields, validates GSTIN and vendor data, predicts GL and tax treatment, then syncs clean entries to Tally or Zoho Books. It also performs GSTR-2B reconciliation and flags duplicates, accelerating close while preserving controls.