Key Takeaways

- The last date of TDS return filing depends on the quarter, not a single annual deadline

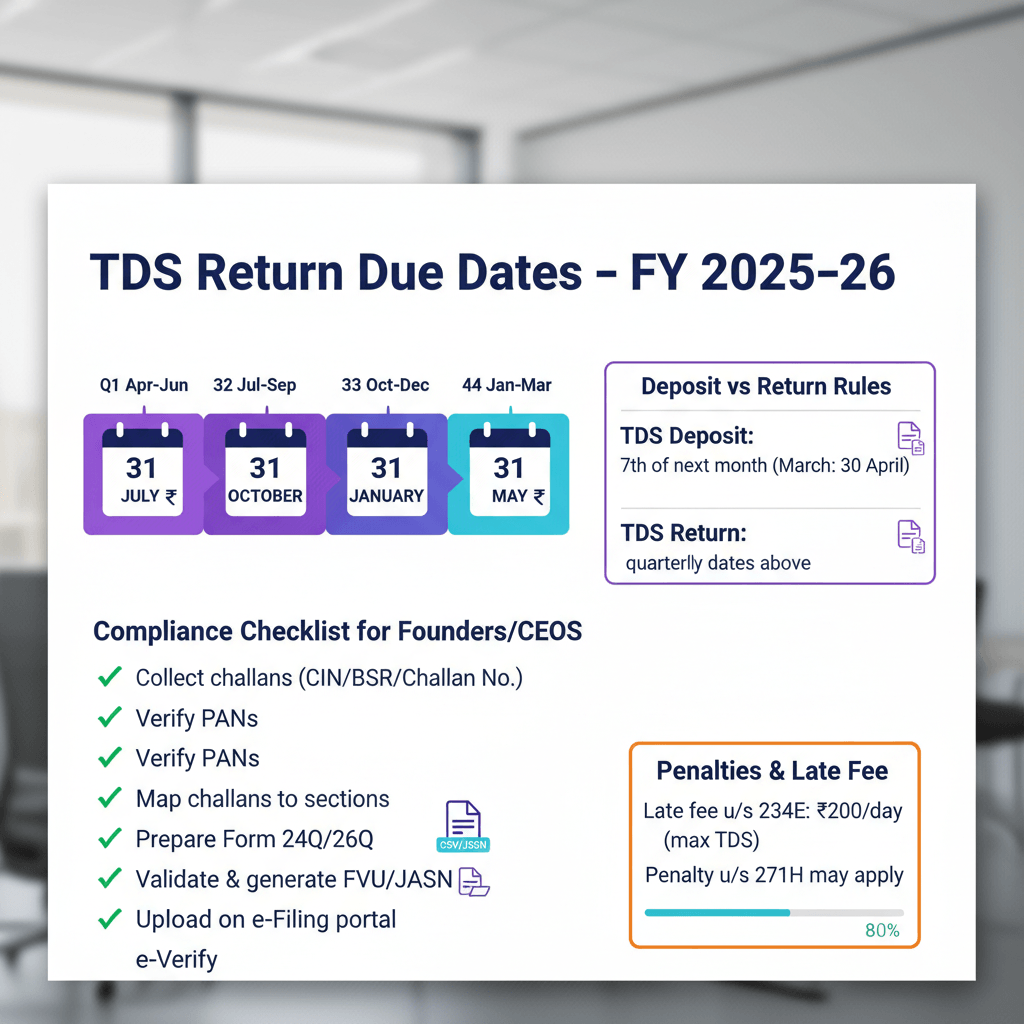

- Q1 (April–June): 31 July | Q2 (July–September): 31 October | Q3 (October–December): 31 January | Q4 (January–March): 31 May

- Applies to Form 24Q (salary), Form 26Q (non-salary resident), Form 27Q (non-resident payments), Form 27EQ (TCS)

- Late filing fee: ₹200 per day under Section 234E, starts automatically the day after the due date, no notice required

- TDS deposit deadline (7th of the following month) is a completely separate obligation from the TDS return filing deadline

- Missing either triggers separate penalties, you can be hit on both counts independently

- Q4 gets an extended deadline to 31 May (not 30 April), this is the most commonly missed date

The Exact Last Date To File TDS Return, All Four Quarters

The last date of TDS return filing in India is not one date, it changes every quarter. Q1 closes on 31 July, Q2 on 31 October, Q3 on 31 January, and Q4, the March quarter, on 31 May of the following year. Miss any of these and the penalty clock starts ticking automatically at ₹200 per day, no notice, no grace period.

Most business owners confuse two separate obligations, when TDS must be deposited with the government, and when the return must be filed. These are different deadlines. You can be compliant on one and non-compliant on the other.

If you are handling TDS compliance in-house, this post gives you every deadline, every penalty, and the exact filing process, nothing theoretical, everything you can act on today. Businesses that outsource this to a service like Virtual Accounting never face this scramble, but if you are managing it yourself, here is exactly what you need to know.

| Quarter | Period | Last Date To File TDS Return |

|---|---|---|

| Q1 | April 1 – June 30, 2025 | 31 July 2025 |

| Q2 | July 1 – September 30, 2025 | 31 October 2025 |

| Q3 | October 1 – December 31, 2025 | 31 January 2026 |

| Q4 | January 1 – March 31, 2026 | 31 May 2026 |

These dates apply to Form 24Q, 26Q, 27Q, and 27EQ, all four major TDS and TCS return forms. The form type does not change the deadline.

The last date for TDS return in Q4 is 31 May, not 30 April. This is the most common mistake. A lot of founders and finance teams mark 30 April in their calendar because March is financial year-end and assume the return is due right after. It is not. The Income Tax Department gives deductors until 31 May specifically because the March quarter involves finalising accounts, computing last-month salary adjustments, reconciling advance tax, and closing the books. The extra month is intentional.

The last date to file TDS return for government deductors follows the same quarterly schedule. Where government entities differ is on the deposit side, when TDS is paid via book entry, rather than challan, it must be deposited on the same day of deduction. But for the return filing itself, the quarterly dates above apply to government deductors as well.

Note: CBDT occasionally issues circulars extending specific quarter deadlines. Always verify the Q4 deadline against the latest CBDT notification before the 31 May filing date, particularly during budget or election years.

TDS Deposit Deadline Vs. TDS Return Filing Deadline, Know The Difference

These are two completely different compliance obligations. Confusing them is the single biggest reason business owners receive unexpected penalty notices.

TDS deposit means paying the TDS you collected to the government via Challan 281. This must happen by the 7th of the following month for every month. So TDS deducted in July must reach the government by 7 August, TDS deducted in September by 7 October, and so on.

The one major exception: TDS deducted in March must be deposited by 30 April, not 7 April. This extended deposit deadline for March applies across all deductors. It is the only month with a deposit window beyond the standard 7-day rule.

TDS return filing is the quarterly statement you submit to the Income Tax Department declaring every deduction made, with deductee PAN details, challan numbers, and payment breakdowns. This comes after all deposits for the quarter are done.

Here is a concrete example. Say you run a Delhi-based consulting firm and deduct TDS in August:

- TDS deducted in August → deposit by 7 September

- That transaction gets reported in the Q2 return, July–September → return filed by 31 October

Both are separate obligations. A business can miss the 7 September deposit deadline while still filing the October return on time. The deposit penalty and the return penalty are levied independently under different sections of the Income Tax Act.

The last date for filing TDS return is always the quarterly deadline. The deposit deadline is monthly. Keeping a simple two-column calendar, one column for deposit dates, one for return filing dates, eliminates most confusion.

Which TDS Return Form Do You File, And Does The Deadline Change?

All four forms follow the same quarterly deadline. Choosing the wrong form is a different problem, but the due date will not shift regardless of which form applies to you. Here is a quick breakdown:

Form 24Q covers TDS on salary payments under Section 192. If you are an employer deducting tax from employee salaries, this is your form. Filed quarterly, same deadlines as the table above. Every company with payroll files this.

Form 26Q covers TDS on all non-salary payments to Indian residents. Contractor payments, Section 194C, professional fees, Section 194J, rent, Section 194I, interest, Section 194A, commission, Section 194H, purchase of goods above ₹50 lakh in a year, Section 194Q, all of these go here. Most SMEs and startups primarily deal with 26Q alongside 24Q.

Form 27Q is for TDS on payments to non-residents and foreign companies. Royalties, technical service fees, interest on foreign loans, if your Bengaluru SaaS company is paying a US software vendor or a UK consultant, 27Q is what you file. Same quarterly deadlines apply.

Form 27EQ is for TCS, Tax Collected at Source. If you are a seller collecting TCS on goods sales above ₹50 lakh to a buyer in a financial year, Section 206C(1H), or on vehicles above ₹10 lakh, scrap, alcohol, or foreign remittances under the Liberalised Remittance Scheme, this is your form. TCS returns follow identical quarterly deadlines to TDS returns. Manufacturing and trading businesses often overlook this.

Form 27A is a control chart or summary document submitted alongside the e-TDS return. It is not a standalone return. It summarises total TDS amounts and challan details, and must be physically signed if submitted at a TIN Facilitation Centre.

Important carve-out: Form 26QB, TDS on property purchase, Form 26QC, TDS on rent paid by individuals, and Form 26QD, contractor payments by individuals or HUFs, work on a transaction-specific deadline, 30 days from the end of the month in which TDS was deducted. These are not quarterly filings and are handled separately from the standard TDS return cycle.

Penalties For Missing The Last Date Of Filing TDS Return

This section is where most people underestimate the real cost of delay. There are three separate penalty mechanisms, and they can stack.

Section 234E — Late Filing Fee

₹200 per day for every day after the due date until the return is actually filed. No notice required. No discretion. It triggers automatically.

The fee is capped at the total TDS amount reported in that return, so if you deducted ₹30,000 in a quarter, the maximum 234E fee is ₹30,000, not unlimited.

⚠️ Warning: Section 234E is not a penalty that can be argued away. It is a mandatory fee under the statute. The Income Tax Department has no power to waive it, and courts have consistently upheld this. Budget for it the moment you miss the deadline.

Real example: A Mumbai D2C brand deducts ₹50,000 TDS in Q2 and misses the 31 October deadline by 60 days.

- Section 234E fee = 60 × ₹200 = ₹12,000

- This is within the ₹50,000 cap, so the full ₹12,000 applies

Section 271H — Discretionary Penalty

A penalty of ₹10,000 to ₹1,00,000 for failing to file a TDS return or filing one with incorrect information. This is levied at the Assessing Officer’s discretion, unlike 234E, it does not apply automatically.

There is a provision to avoid 271H: if the deductor pays the TDS amount due, files the return within one year of the due date, and pays all 234E fees plus applicable interest, the 271H penalty can be avoided. This is the only legitimate escape route from the discretionary penalty.

Section 201(1A) — Interest On Late TDS Deposit

This applies to the deposit obligation, not the return filing, but worth knowing because both can be triggered in the same failure scenario:

- 1% per month, or part of month, from the date TDS was deductible to the date it was actually deducted

- 1.5% per month, or part of month, from the date TDS was deducted to the date it was actually deposited

Both rates apply on simple interest, calculated month-by-month including partial months.

Section 276B — Prosecution

In extreme cases where TDS was deducted from employees or vendors but never deposited with the government, prosecution can be initiated. Imprisonment of 3 months to 7 years, along with a fine. This is not theoretical, the Income Tax Department has pursued prosecution against habitual defaulters and company directors.

The last date of filing TDS return matters not just for the fee, but because late filing delays Form 16A generation, blocks deductees from claiming TDS credit in their own ITR, and can cascade into complaints from vendors and employees during ITR filing season.

Who Must File TDS Returns, Are You Actually Obligated?

Anyone who holds a TAN, Tax Deduction Account Number, and has deducted TDS in a quarter is required to file a TDS return for that quarter. TAN registration is done via Form 49B and is a prerequisite, no TAN, no return filing, and no legal deduction.

Mandatory deductors include:

- All companies, private, public, OPC, regardless of size

- Partnership firms and LLPs

- Individuals and HUFs whose accounts are subject to tax audit under Section 44AB

- All government entities, central, state, and local bodies

Individuals and HUFs not under tax audit are generally not required to file quarterly TDS returns, with two exceptions: when deducting TDS on monthly rent exceeding ₹50,000, Section 194-IB, handled via Form 26QC, a transaction-specific process, not a quarterly return, or certain contractor or professional payments in specific situations.

If no TDS was deducted in a quarter, for example, a startup that had no vendor payments triggering TDS thresholds, there is currently no statutory mandate to file a NIL TDS return. However, if your TAN is active and you have historically filed returns, a NIL return is considered best practice to keep your compliance record clean and avoid queries.

One operational point: deductee PAN accuracy is non-negotiable. If you report a wrong or missing PAN for a vendor or employee, TDS is applicable at 20% flat instead of the standard rate. More importantly, the deductee cannot claim credit for that TDS in their ITR until the return is corrected on TRACES.

How To File Your TDS Return Before The Last Date, The Actual Process

Filing a TDS return is a multi-step process. Here is the sequence, in order:

Step 1: Confirm TDS deposits are complete. All TDS for the quarter must be deposited via Challan 281, through net banking or an authorised bank. Save the BSR code, bank branch code, and challan serial number for every deposit. These are mandatory fields in the return.

Step 2: Compile deductee data. For every payment where TDS was deducted, contractor, vendor, employee, you need the PAN, payment amount, TDS amount, and challan reference. This is where missing or incorrect PANs show up and slow down the process.

Step 3: Prepare the return using the RPU, Return Preparation Utility. NSDL provides a free Return Preparation Utility. Enter all deductee details, challan details, and payment data. The tool generates the return file in the required format.

Step 4: Validate using the FVU, File Validation Utility. Run the generated file through the FVU, also available from NSDL. It checks for errors, mismatches, and missing fields before you submit. Fix all errors flagged at this stage before proceeding.

Step 5: Submit the validated .fvu file. Online submission is the standard route, through the TIN e-filing system or the Income Tax e-filing portal using your TAN login. Larger deductors with high transaction volumes may use a TIN Facilitation Centre.

Step 6: Submit Form 27A. This signed control chart accompanies the .fvu file. For online submissions, the digital equivalent is uploaded alongside the return.

Step 7: Save the acknowledgement. The system issues a token number or provisional receipt number confirming successful submission. Keep this for your records, it is your proof of filing.

Practical tip: Start data compilation by the 15th of the due month, 15 July for Q1, 15 October for Q2, 15 January for Q3, 15 May for Q4. TRACES and TIN portals tend to slow significantly in the last 48 hours before any filing deadline. Companies handling 200+ transactions across multiple vendors every quarter often find outsourcing this process, including to managed finance services, more cost-effective than maintaining the in-house bandwidth.

TDS Return Deadlines And TDS Certificate Issuance, What Comes Next

Filing the return is not the end of the TDS cycle. After the return is processed on TRACES, the deductor has a statutory obligation to issue TDS certificates to deductees.

| Certificate | Form | Source | Deadline |

|---|---|---|---|

| Salary TDS certificate | Form 16 | Filed via 24Q | 15 June of the following financial year |

| Non-salary TDS certificate | Form 16A | Filed via 26Q / 27Q | 15 days from the quarterly return due date |

Form 16A deadlines by quarter:

- Q1: by 15 August

- Q2: by 15 November

- Q3: by 15 February

- Q4: by 30 June, 15 days from 31 May

Both Form 16 and Form 16A can only be generated through the TRACES portal. They are digitally signed and downloaded directly from TRACES after the return is processed. You cannot create these manually.

Failure to issue Form 16 or 16A on time carries a penalty of ₹100 per day per certificate under Section 272A(2)(g). For a company with 50 vendors, that adds up fast.

More practically: your vendors and consultants need Form 16A to file their own ITR. If you issue it late, their ITR gets delayed or filed without claiming credit for TDS you deducted from them. This creates disputes, damages vendor relationships, and in some cases triggers complaints to the Income Tax Department.

Special Cases, March Quarter, Corrections, And Lower Deduction Certificates

Correction Returns

Errors happen, a wrong PAN, an incorrectly entered TDS amount, a mismatched challan. A correction return filed on TRACES updates the original return and fixes the deductee’s Form 26AS and AIS entries.

There is no hard statutory deadline for corrections beyond a 6-year window from the end of the relevant financial year. After that, corrections cannot be processed. Operationally, file corrections as soon as an error is identified, every month it sits uncorrected, a vendor or employee is unable to claim their TDS credit.

March Quarter Specifics

- TDS deducted in March → deposit by 30 April

- Q4 TDS return, January–March → file by 31 May

These are not the same date. Deposit and return filing for the March quarter each have their own extended deadline.

Lower or Nil Deduction Certificates Under Section 197

A payee, typically a vendor or contractor, can approach their Assessing Officer for a certificate authorising TDS at a lower or nil rate. The certificate is issued via Form 13 and is valid for the financial year specified.

If you receive such a certificate from a vendor, you deduct TDS at the lower rate stated in the certificate. You still include these transactions in your TDS return, recording the certificate number against the deductee’s PAN. Failure to capture the certificate number can result in TDS credit mismatches for the deductee.

TCS Returns, Form 27EQ

TCS returns follow the exact same quarterly deadlines as TDS returns. If you are a manufacturer selling goods to buyers exceeding ₹50 lakh in a financial year, Section 206C(1H), or dealing in scrap, minerals, timber, alcohol, or vehicles above ₹10 lakh, TCS compliance is mandatory. Many trading businesses discover this obligation only after receiving a notice. The quarterly return deadline calendar is identical to TDS.

Closing, Managing TDS Deadlines Without Burning Internal Bandwidth

TDS compliance is not complex, but it is relentless. Four return deadlines, monthly deposit obligations, Form 16 and 16A issuances, correction return management, and TRACES reconciliation happening simultaneously across 12 months.

If managing this cycle is pulling your finance team away from growth-critical work, Virtual Accounting handles the entire TDS compliance stack, deposits, return filing across all forms, Form 16/16A generation on TRACES, and correction returns, as part of its managed accounting service starting at ₹4,000/month. Details.

Frequently Asked Questions

What Is The Last Date Of TDS Return For Q4, January To March?

The last date to file the Q4 TDS return is 31 May of the following year. For FY 2025–26, that is 31 May 2026. This is not 30 April, the extra month is intentional because the March quarter involves account finalisation and year-end reconciliation.

Is The TDS Deposit Deadline And TDS Return Deadline The Same?

No. TDS must be deposited by the 7th of the following month, or 30 April for March deductions. The TDS return is filed quarterly, by 31 July, 31 October, 31 January, or 31 May. These are separate obligations with separate penalties.

What Happens If I Miss The Last Date For TDS Return Filing?

Section 234E applies immediately, ₹200 per day from the day after the due date until the date of actual filing, capped at the total TDS for that quarter. Separately, Section 271H allows a discretionary penalty of ₹10,000 to ₹1,00,000 for late or incorrect returns. If you have already missed the date, pay outstanding TDS and interest, file within one year of the due date, and settle the 234E fee to avoid 271H. If internal bandwidth is tight, Virtual Accounting by AI Accountant can handle the catch-up filing, data validation, and TRACES corrections end-to-end.

Does The TDS Return Deadline Change Based On Which Form I File?

No. Form 24Q, 26Q, 27Q, and 27EQ all follow the same quarterly due dates. The form type does not extend or shorten the deadline.

Am I Required To File A NIL TDS Return If I Made No Deductions In A Quarter?

There is no statutory mandate to file a NIL TDS return. However, if your TAN is active and you have filed previously, a NIL return is best practice to avoid queries and maintain a clean compliance trail on TRACES.

What Is Section 234E And Can It Be Waived?

Section 234E imposes a mandatory late filing fee of ₹200 per day. It is not discretionary. It is capped at the total TDS deducted for that quarter, but once accrued, it cannot be waived by the department or courts.

What Is The Deadline To Issue Form 16A To Vendors After Filing The TDS Return?

Form 16A must be issued within 15 days of the quarterly return due date. For Q1 that is 15 August, Q2 is 15 November, Q3 is 15 February, and Q4 is 30 June. Form 16A is generated only through TRACES after the return is processed.

What Is The Due Date To Deposit TDS Deducted In March?

TDS deducted in March must be deposited by 30 April, not 7 April. March is the only month with an extended deposit window.

Do Individuals Need To File TDS Returns?

Individuals and HUFs not subject to tax audit under Section 44AB generally do not file quarterly TDS returns. Exceptions include TDS on rent above ₹50,000 per month under Section 194-IB, handled via Form 26QC, and certain specified transactions.

What Is Form 27A And Is It Mandatory?

Form 27A is a control chart submitted with the e-TDS return. It summarises total TDS and challan details and accompanies the .fvu file. It is mandatory and does not replace the quarterly return.

How Do I Correct Errors Like Wrong PAN Or Challan Mismatch After Filing?

File a correction return on TRACES. Update the deductee PAN, challan reference, or amounts as needed. There is an operational window of up to six years from the end of the relevant financial year, but correct as soon as possible so deductees’ Form 26AS and AIS reflect accurate credit.

Can I File A TDS Return Without A TAN?

No. A valid TAN is mandatory to deduct TDS and to file TDS returns. Apply using Form 49B first, then proceed with deposit and return filing. Using a PAN in place of TAN for TDS returns is not permitted.

What If My Team Cannot Handle The Quarterly Crunch Before The Due Date?

Implement a mid-quarter reconciliation routine, lock PAN collection early, and begin RPU data prep by the 15th of the due month to avoid last-minute portal slowdowns. If internal capacity is a constraint, Virtual Accounting by AI Accountant can manage deposits, return preparation, FVU validation, e-filing, and certificate issuance so you meet every deadline reliably.