Key Takeaways

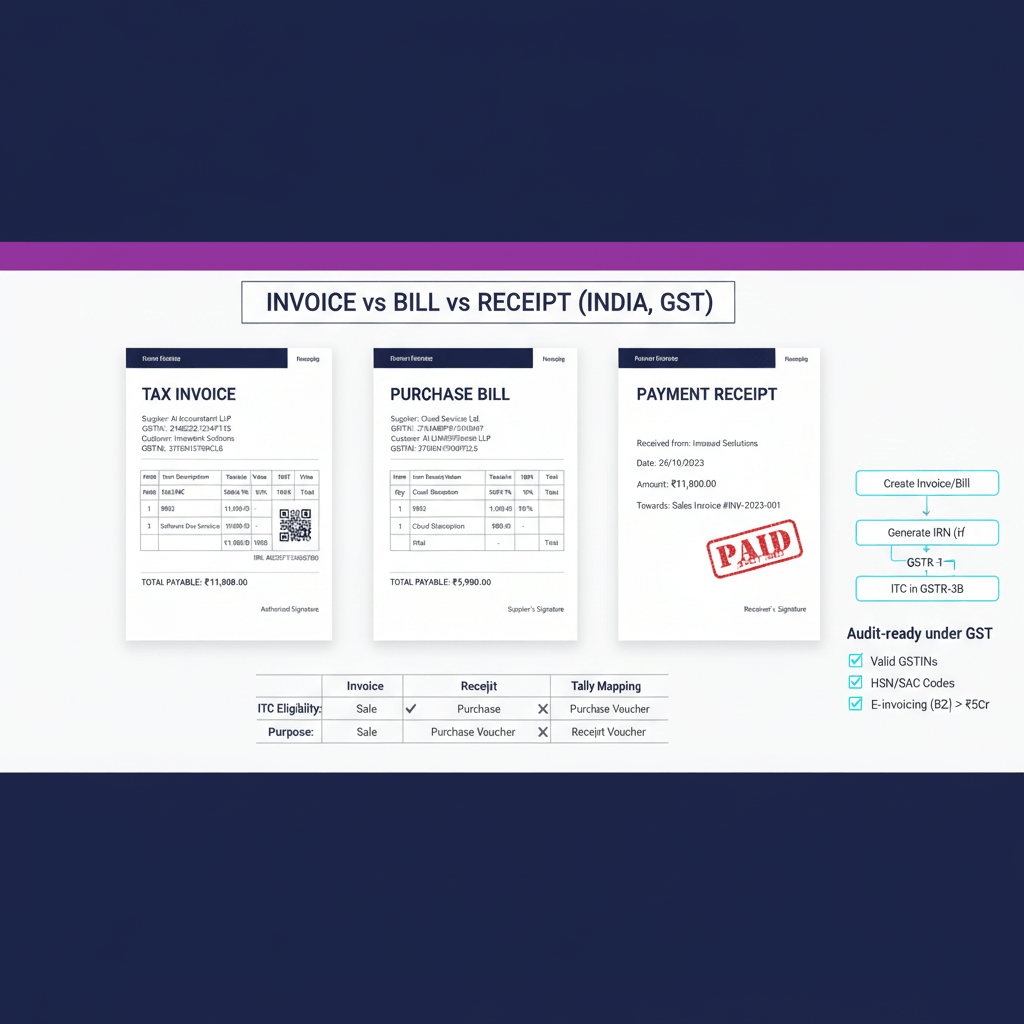

Invoice vs Bill vs Receipt, the short answer

They are not interchangeable. Under Section 31 of the CGST Act, 2017 and the CGST Rules, you deal with three different families of documents, each with unique fields and effects on ITC and e-invoicing.

The most common and costly mistake, calling a vendor’s tax invoice a “bill of supply,” then posting it as exempt, silently blocks ITC and corrupts your GSTR-2B reconciliation.

Invoice and bill under GST, the legal difference

Tax invoice, the seller’s statutory demand

A tax invoice is mandatory for taxable supplies under Section 31 of the CGST Act, 2017. Rule 46 lists 16 fields, including supplier and recipient details, GSTINs, consecutive serial number, date, HSN or SAC, taxable value, tax rate, CGST, SGST or IGST, and signature. For B2B supplies where aggregate turnover exceeds ₹5 crore, the invoice must carry IRN and QR code, as notified in CBIC Notification No. 10/2023 – Central Tax. Without IRN, Rule 48(5) makes the document invalid as a tax invoice.

Bill of supply, a different document, not a synonym

Issued for exempt supplies or by composition dealers per Section 31(3)(c), the bill of supply has identification fields, but no tax rate or tax amount under Rule 49. It generates no ITC, it is not e-invoice eligible, and in Tally it should be recorded as an exempt Sales entry, never a taxable Purchase with ITC.

Receipt, a payment acknowledgement, not evidence of supply

A receipt voucher under Section 31(3)(d) is issued when you receive an advance. It acknowledges movement of money, not the supply. It cannot substitute a tax invoice at the time of supply, and it does not by itself create ITC for the payer.

Where misclassification breaks GST compliance

ITC blocked because the purchase was posted wrong

Section 16(2)(aa) ties ITC to whether an invoice appears in GSTR-2B, the auto drafted, static statement for the month. If your team books a vendor’s invoice as a Receipt, Journal, or an expense without GST, Tally will not include it in the GST purchase register, and you will not see it in the GSTR-3B flow. The GSTR-2B match fails, credit remains blocked.

E-invoice omission makes the invoice invalid

Above ₹5 crore turnover, a B2B invoice without IRN is invalid under Rule 48(5). The issuer risks a penalty of ₹10,000 or 100 percent of the tax due per invoice, whichever is higher, under Section 122, and the recipient’s ITC collapses because an invalid document cannot populate GSTR-2B.

Bill of supply posted as taxable purchase creates phantom ITC

If an exempt bill of supply is posted with GST, Tally computes credit that does not exist. Claiming it in GSTR-3B triggers reversal and interest at 24 percent per annum under Section 50(3), with potential penalties.

Advance and receipt chain broken, refund voucher missed

Booking a customer advance as a Sales invoice, instead of a Receipt voucher with bill wise reference, leaves both a receivable and a credit in the ledger, and breaks the Section 31(3)(d) receipt voucher requirement. If the deal collapses, the refund voucher under Section 31(3)(e) and Rule 51 is missed, and tax reversal timing goes wrong.

If vendors send mixed or mislabeled templates, bulk ingestion and auto classification can prevent errors at source. For example, vendor bill classification and matching standardizes Rule 46 fields, tags GST treatment correctly, and posts clean Purchase vouchers to Tally.

Tally Prime mapping, the one time setup that fixes everything

Activate bill wise details

In Gateway of Tally, F11, Accounting Features, enable “Maintain Bill wise Details.” You will see four reference types on allocation, New Ref, Agst Ref, Advance, On Account. New Ref creates an outstanding, Agst Ref settles a specific invoice. Without it, ageing and reconciliations drift.

Outward supplies, Sales voucher

Use Sales for all taxable outward supplies. Ensure party GSTIN, correct HSN or SAC, and tax rate on items or service ledgers. If turnover exceeds ₹5 crore, enable e invoice in Tally so the IRN and QR code are fetched from the IRP. For exempt supplies, set taxability to Exempt, the output becomes a bill of supply under Rule 49, and e invoicing does not apply, as clarified in CBIC Notification No. 13/2020 – Central Tax.

Inward supplies, Purchase voucher

Every vendor tax invoice, regardless of what it is called, goes to Purchase. Enter vendor GSTIN, supplier invoice number and date, allocate HSN or SAC, and GST rate. Use New Ref with the vendor’s invoice number. When paying, use a Payment voucher with Agst Ref to close the outstanding. Before claiming ITC, verify that the invoice appears in GSTR-2B for the period, per Section 16(2)(aa). For process control, see GSTR-2B reconciliation.

RCM entries, self invoice and payment voucher

For supplies from unregistered persons covered by RCM, issue a self invoice at receipt of supply under Section 31(3)(f), then a payment voucher at payout under Section 31(3)(g). In Tally, mark the Purchase as RCM, book tax as payable, then raise a Payment voucher to the vendor with Agst Ref. Pay the RCM via the cash ledger in GSTR-3B, then claim eligible credit in the same period if used for business.

To remove manual effort, use bookkeeping automation that predicts ledgers from bank and card lines, posts Purchase entries consistently, and flags invoices missing in GSTR-2B.

Five scenarios that cover ninety percent of questions

1. You ship goods to a registered buyer

Document: Tax invoice, B2B. Tally: Sales, New Ref to create receivable. If above ₹5 crore turnover, generate IRN first, per CBIC Notification No. 10/2023 – Central Tax, otherwise the invoice is invalid under Rule 48(5).

2. You receive a service invoice from a registered vendor

Document: Tax invoice received, vendor bill. Tally: Purchase, New Ref with supplier invoice number, ITC booked. Claim only if it appears in GSTR-2B for that month, per Section 16(2)(aa).

3. You pay an unregistered freelancer

Document: Self invoice under RCM, then payment voucher. Tally: RCM flagged Purchase to book liability, Payment voucher to settle the freelancer. Example, legal fee ₹1,00,000, GST 18 percent, ₹18,000 RCM payable, then eligible for ITC if used for business.

4. You receive a ₹2,00,000 customer advance

Document: Receipt voucher under Section 31(3)(d). Tally: Receipt with Advance reference. If GST applies on advances, compute tax on advance. On supply, raise tax invoice and adjust advance. If cancelled, issue refund voucher under Rule 51 and reverse tax.

5. You supply exempt goods

Document: Bill of supply under Rule 49. Tally: Sales with Exempt taxability, no GST, no e invoice. If posted by mistake as taxable, output tax inflates and needs correction in GSTR-1.

Two week checklist to lock terminology and mapping

Week one, fix masters and templates

Week two, train, template, automate

Pro tip: Teach one rule in onboarding, “Every supplier tax invoice is a Purchase voucher with vendor GSTIN and New Ref,” most downstream ITC problems disappear.

FAQ

Is a tax invoice and a bill the same under GST, or are they different documents?

They are different. A tax invoice is a statutory document under Section 31 and Rule 46, with 16 mandatory fields and, where applicable, an IRN. “Bill” is colloquial. The Act defines a bill of supply for exempt or composition supplies under Section 31(3)(c), which carries no GST and yields no ITC. Your internal “vendor bill” is simply a supplier’s tax invoice posted as a Purchase voucher.

Can I claim ITC on a proforma invoice or on a receipt voucher?

No. A proforma invoice is not a tax invoice under Section 31, and a receipt voucher merely acknowledges payment under Section 31(3)(d). ITC is available only when a valid tax invoice is issued and the credit appears in your GSTR-2B, as required by Section 16(2)(aa).

What happens if a supplier above ₹5 crore turnover issues a B2B invoice without IRN?

The document is invalid as a tax invoice under Rule 48(5). You should not claim ITC, and the supplier risks a penalty of ₹10,000 or 100 percent of tax due per invoice under Section 122. Ask for cancellation and re-issue with IRN, confirmed at the IRP per CBIC Notification No. 10/2023 – Central Tax.

We mistakenly posted a bill of supply as a taxable Purchase in Tally, how do we fix it?

Reverse the entry, remove GST allocation, and re-post as an expense or exempt purchase. If ITC was claimed in GSTR-3B, reverse it with 24 percent interest under Section 50(3), then correct the current period’s registers.

Is a vendor bill in Tally the same as a bill of supply?

No. A vendor bill is your inward tax invoice from a registered supplier, posted as a Purchase voucher with GST, enabling ITC. A bill of supply is for exempt or composition supplies and carries no GST. Conflating the two either blocks credit or creates wrongful credit.

Do debit notes and credit notes require e-invoicing for eligible taxpayers?

Yes. Debit notes and credit notes related to B2B supplies require IRN generation for taxpayers above the threshold, the same invalidity and penalty rules apply if IRN is missing.

How should I record customer advances and subsequent adjustments in Tally?

Record a Receipt voucher with an Advance reference when money is received. On raising the tax invoice, use Agst Ref to adjust the advance. If the deal is cancelled, issue a refund voucher under Rule 51 and reverse the tax in the next return.

Can a composition dealer issue a tax invoice and collect GST?

No. Composition dealers must issue a bill of supply and cannot collect GST. If they do, penalties apply and the GST collected must still be deposited. The recipient cannot claim ITC on such supplies.

What documents must I insist on from vendors to safely claim ITC?

A valid tax invoice per Rule 46 with vendor GSTIN, your GSTIN, consecutive serial number, HSN or SAC, taxable value, and GST split. If the vendor is above ₹5 crore turnover, the invoice must carry IRN and QR code per CBIC Notification No. 10/2023 – Central Tax. Finally, confirm the invoice appears in your GSTR-2B before claiming credit.

How do I handle a mixed invoice containing both taxable and exempt items?

Post as a single Purchase voucher with split allocation, taxable lines to GST ledgers, exempt lines to exempt ledgers. If inputs are used for both taxable and exempt outputs, evaluate Rule 42 for proportionate ITC reversal. If the supplier has not separated values, request an invoice cum bill of supply under Rule 46A before posting.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.