Key Takeaways

• The core difference: GSTR-2A is a live record that updates whenever a supplier files or amends a return, while GSTR-2B is a static monthly statement, frozen on the 14th, that fixes the Input Tax Credit you can claim for that period. Use 2A to track suppliers through the month, and 2B to claim ITC in your GSTR-3B.

• Compliance is up, but gaps remain: On-time GSTR-3B filing rose from around 68% in 2017-18 to roughly 90% in 2022-23. Even so, millions of returns are filed late each year, so a single slow supplier can still delay the credit you are owed.

• What businesses struggle with: In conversations with over 2,100 businesses, 827 named supplier compliance tracking as a major pain point, with finance teams spending a day or two each month just validating whether vendors had filed. Your ITC depends on suppliers you do not control.

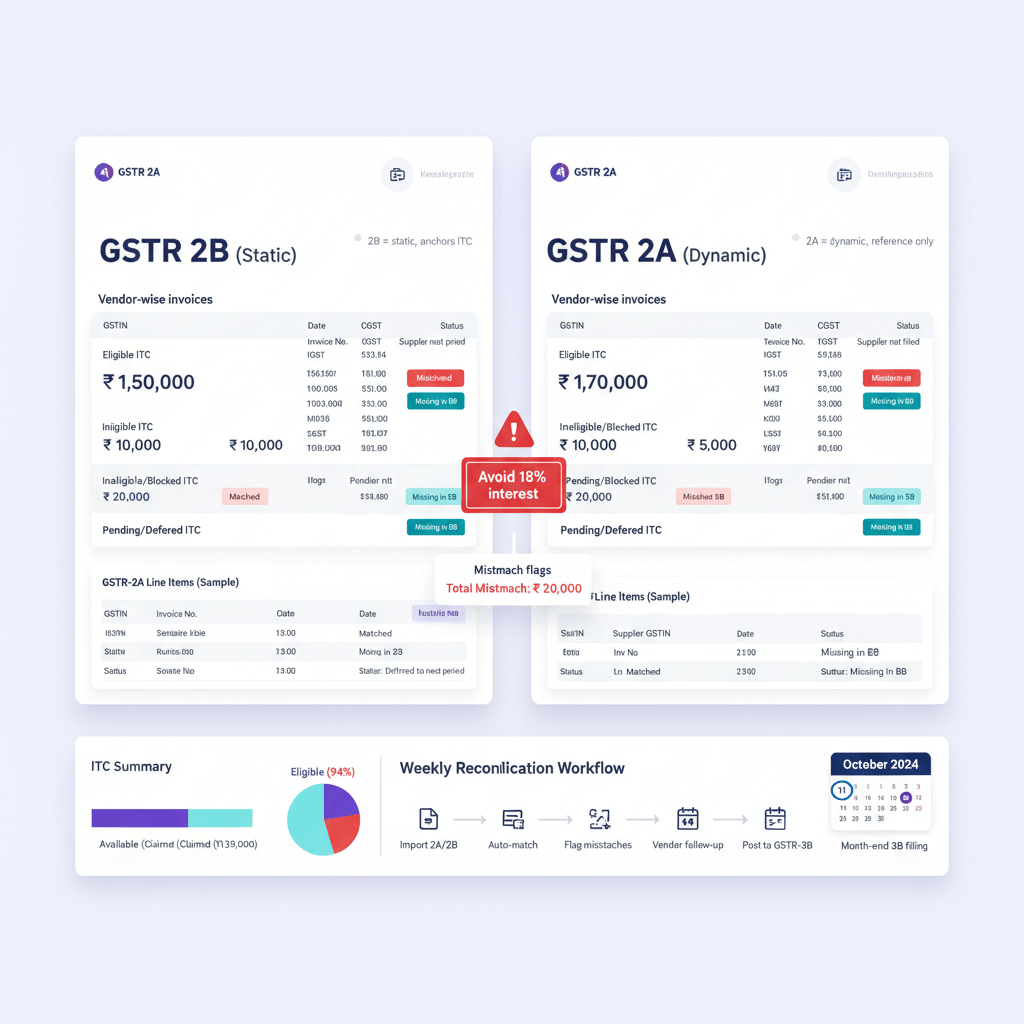

• How tools like AI Accountant help: By continuously matching your Tally purchase register against your live GSTR-2A and frozen GSTR-2B, AI Accountant flags missing invoices, non-filing suppliers, and mismatches automatically, so you catch issues early and protect your ITC instead of hunting for them by hand.

Quick Overview: What Is the Difference Between GSTR-2A and GSTR-2B?

GSTR-2A and GSTR-2B are auto-generated purchase records available on the GST portal. Both forms show details of purchases reported by your suppliers.

The core difference is:

• GSTR-2A is a live, continuously updated record of your purchases. It changes whenever a supplier files or amends their GSTR-1.

• GSTR-2B is a static monthly statement that shows the Input Tax Credit (ITC) available for a specific return period. Once generated, it does not change, making it the reference document for claiming ITC.

The key difference is how and when the data is updated. GSTR-2A is a live purchase record that updates whenever suppliers file or amend GST returns, whereas GSTR-2B is a fixed monthly ITC statement that shows the Input Tax Credit available for a specific return period.

Why do GSTR-2A and GSTR-2B show different figures?

Because GSTR-2A updates whenever suppliers file or amend returns, while GSTR-2B captures data only up to a specific cut-off date for a particular return period. If a supplier files after that cut-off, the invoice may appear in GSTR-2A immediately but only appear in GSTR-2B in a later period. This difference is normal and does not indicate an error.

What is GSTR-2A?

GSTR-2A is a dynamic, auto-generated purchase statement available on the GST portal. It shows all purchase invoices that your suppliers have reported against your GSTIN through their GST returns, primarily GSTR-1.

Whenever a supplier uploads, modifies, or corrects an invoice, the changes automatically appear in your GSTR-2A.

The biggest use of GSTR-2A is reconciliation. In practice, businesses match the invoices in their purchase register against the invoices appearing in GSTR-2A and investigate any differences before filing GST returns.

Businesses use GSTR-2A to identify missing invoices, incorrect GST amounts, or suppliers who have not filed their returns.

For example, suppose your purchase register for April shows purchases from 12 suppliers. When you review GSTR-2A during April or early May, only 9 suppliers appear. This immediately tells you one of these things:

• Some suppliers have not filed GSTR-1 yet

• Certain invoices have not been uploaded

• Invoice details have been entered incorrectly

Instead of discovering these issues while filing GST returns, you can identify them early and follow up with suppliers before the month closes.

How AI Accountant Automates GSTR-2A Reconciliation

Tracking GSTR-2A manually means doing four things, repeatedly, every month:

• comparing your purchase register against the GST portal,

• checking which suppliers have filed,

• identifying missing invoices, and

• following up with vendors, repeatedly.

.png)

We have spoken to over 2,100 businesses so far, and out of them, 827 business owners and finance professionals mentioned supplier compliance tracking as a major pain point. It is one of the most common problems we hear, across manufacturing, construction, CA firms, retail and real estate businesses.

AI Accountant automates this process by continuously matching your Tally purchase register with your live GSTR-2A data. Instead of manually hunting for discrepancies, you get alerts when there is one.

Rather than logging into the GST portal multiple times a month, finance teams can monitor supplier compliance from a single dashboard. By identifying issues early, businesses have more time to follow up with vendors and ensure eligible invoices are reflected before ITC claims are affected.

Is GSTR-2A still relevant now that GSTR-2B exists?

Yes. While businesses typically use GSTR-2B for ITC claims, GSTR-2A remains valuable for ongoing reconciliation and supplier monitoring. It helps you identify missing invoices and non-compliant suppliers before the return filing deadline.

Do I have to file GSTR-2A?

No. GSTR-2A is automatically generated by the GST portal using data reported by your suppliers. It is a view-only statement that you can use for reconciliation and compliance checks. There is no separate filing requirement.

What is GSTR-2B?

GSTR-2B is a static, auto-generated statement available on the GST portal that shows the Input Tax Credit (ITC) available to you for a specific return period.

It uses the same supplier-reported data as GSTR-2A. The difference is that GSTR-2B is generated once for a return period and remains unchanged afterward.

Because the statement is fixed, businesses use it as the primary reference for claiming ITC while filing GSTR-3B.

How GSTR-2B Handles Late Filings and Corrections

Once a GSTR-2B statement is generated, it is never edited retrospectively.

If a supplier files an invoice after the cut-off date, that invoice does not get added to the already-generated GSTR-2B. Instead, it appears in a future GSTR-2B.

The same principle applies to invoice corrections. If a supplier amends an invoice after a period's GSTR-2B has been generated, the adjustment is reflected in a later statement rather than changing the earlier one.

In practice, this means ITC is often delayed rather than lost. Missing invoices and corrections typically flow into future periods once suppliers update their returns.

This is where GSTR-2A becomes important.

Because GSTR-2A updates continuously throughout the month, it helps you identify missing invoices and supplier filing issues before GSTR-2B is generated.

Businesses often use GSTR-2A as an early-warning system and GSTR-2B as the final statement used for claiming ITC.

A simple way to think about it is:

- GSTR-2A tells you what suppliers are reporting right now

- GSTR-2B tells you what ITC is available for the return period

How Businesses Use GSTR-2B for ITC Claims

The primary purpose of GSTR-2B is to support ITC claims in GSTR-3B.

Businesses typically reconcile their purchase records with GSTR-2B before filing returns. This helps ensure they claim the correct amount of ITC and identify invoices that are missing due to supplier filing delays.

It is also important to remember that ITC cannot be carried forward indefinitely. Under current GST rules, eligible ITC for a financial year must generally be claimed by 30 November of the following financial year or before filing the annual return, whichever is earlier.

How AI Accountant Automates GSTR-2B Reconciliation

Of the businesses we have spoken to, 151 specifically called out GSTR-2B matching as a problem they were actively trying to solve, and the frustration is almost always the same: tiny mismatches that break the match and put their Input Tax Credit at risk.

AI Accountant automates this by matching your Tally purchase register against your frozen GSTR-2B line by line, using intelligent matching that absorbs the differences which break manual and formula-based tools, such as decimal rounding, invoice-number prefixes, and vendor names that don't align exactly. Instead of eyeballing hundreds of rows, you review only the genuine exceptions.

Why does my GSTR-2B show less ITC than I actually paid?

Because GSTR-2B only includes invoices from suppliers who filed before the cut-off. If a supplier files late, that invoice, and your credit on it, moves to the next month's GSTR-2B. The credit is not lost; it just arrives one cycle later.

Do I have to file GSTR-2B?

No. Like GSTR-2A, GSTR-2B is auto-generated by the GST portal from your suppliers' filings. It is a view-only statement that you use as the reference for claiming ITC in your GSTR-3B, but there is no separate filing requirement for GSTR-2B itself.

Where Do GSTR-2A and GSTR-2B Fit in Your Monthly GST Cycle?

GSTR-2A and GSTR-2B sit in the middle of your GST workflow. After suppliers file GSTR-1, the GST portal generates your GSTR-2A and GSTR-2B. You then reconcile these statements against your books before filing GSTR-3B and claiming Input Tax Credit.

.png)

Let's follow a single purchase through the process.

- You purchase goods and provide your GSTIN to the supplier.

- The supplier reports the invoice in their GSTR-1.

- The invoice appears in your GSTR-2A and is later reflected in your GSTR-2B for the relevant return period.

- You reconcile the invoices in GSTR-2B against your purchase records.

- You file GSTR-3B and claim the ITC available to you.

The key step here is reconciliation. This is where you compare the purchases recorded in your accounting system with the invoices reflected in GSTR-2B. Any mismatch could mean a supplier has filed late, entered incorrect details, or not filed at all.

What Happens If My Supplier Does Not File Their GSTR-1?

If a supplier does not file GSTR-1, their invoice will not appear in your GSTR-2B. In most cases, that means you cannot claim Input Tax Credit (ITC) on that purchase until they file.

This is one of the biggest challenges in the GST system. You may have received the goods, paid the invoice, and recorded the transaction correctly, but your ITC still depends on the supplier reporting the invoice.

A related problem is mis-tagging. If a supplier reports your invoice as a B2C (consumer) sale instead of a B2B sale, it cannot be mapped to your GSTIN, so it will not appear in your GSTR-2B even though the supplier did file. The fix is the same as for a wrong GSTIN: ask the supplier to amend their GSTR-1 so the invoice is correctly tagged to your GSTIN.

That is why businesses regularly monitor GSTR-2A and reconcile GSTR-2B against their books. The earlier you identify non-compliant or mis-tagged suppliers, the earlier you can follow up and reduce delays in receiving your credit.

Tools such as AI Accountant help automate this process by continuously matching supplier-reported invoices against your purchase records and highlighting vendors who have not filed or whose invoices are missing.

Can I claim ITC if the invoice is not in my GSTR-2B?

Generally, no. If an invoice is missing from GSTR-2B because the supplier has not filed GSTR-1, you usually need to wait until the supplier files and the invoice appears in a future GSTR-2B before claiming the credit.

GST Compliance Has Improved, But Supplier Filing Delays Still Matter

Since GST was introduced, return filing compliance has improved significantly. According to government data, on-time GSTR-3B filing rates increased from around 68% in 2017-18 to approximately 90% in 2022-23.

.png)

The trend is encouraging, but even with 90% compliance, millions of returns are still filed late every year. For businesses, that means supplier filing delays remain a real risk to timely ITC claims.

This is why GSTR-2A tracking and GSTR-2B reconciliation remain important. The goal is not just compliance. It is making sure the ITC you've already paid for actually reaches your books on time.

Frequently Asked Questions

What is the main difference between GSTR-2A and GSTR-2B?

GSTR-2A is a live purchase statement that updates whenever suppliers file or amend their GST returns. GSTR-2B is a fixed monthly statement that shows the Input Tax Credit (ITC) available for a specific return period. Businesses typically use GSTR-2A for reconciliation and GSTR-2B for claiming ITC.

Do I need to file GSTR-2A or GSTR-2B?

No. Both GSTR-2A and GSTR-2B are automatically generated by the GST portal using data reported by your suppliers. You can view and download them, but you do not file either form.

Which form should I use for claiming Input Tax Credit?

GSTR-2B should be used as the primary reference for claiming ITC. It provides a fixed view of the credit available for a particular return period and is the statement businesses typically rely on when filing GSTR-3B.

Why are my GSTR-2A and GSTR-2B figures different?

This usually happens because GSTR-2A updates continuously while GSTR-2B is generated for a specific return period and then remains unchanged. If a supplier files after the relevant cut-off date, the invoice may appear in GSTR-2A immediately but only show up in a later GSTR-2B.

How does the GST portal know what I purchased?

The GST portal gets this information from your suppliers. When a supplier files GSTR-1 and includes your GSTIN on an invoice, the portal automatically links that invoice to your GST account and reflects it in GSTR-2A and GSTR-2B.

What if a supplier never files GSTR-1?

If a supplier does not file GSTR-1, the invoice generally will not appear in your GSTR-2B. As a result, your ability to claim ITC on that purchase may be affected until the supplier files the return. This is why businesses regularly monitor supplier compliance and reconcile their purchase records.

Why does my GSTR-2B show less ITC than I actually paid?

A common reason is delayed supplier filing. You may have paid GST and recorded the purchase in your books, but if the supplier has not filed the invoice within the relevant period, the credit may not appear in that month's GSTR-2B. The ITC is often reflected in a later period once the supplier files.

What happens if my supplier enters the wrong GSTIN?

If your GSTIN is entered incorrectly, the invoice may not appear in your GSTR-2A or GSTR-2B. Until the supplier corrects the invoice details, the GST portal cannot link that purchase to your account, which can delay your ITC claim.

Is there a deadline to claim my ITC?

Yes. The ITC for a financial year must be claimed by 30 November of the following financial year, or the date of filing your annual return, whichever is earlier. After that date, any unclaimed ITC is permanently lost, so it is important not to let a supplier's invoice keep slipping from one period to the next indefinitely.

Is reconciling GSTR-2B with my books mandatory?

There is no separate reconciliation return to file, but reconciliation is an important compliance practice. Comparing GSTR-2B with your purchase register helps identify missing invoices, supplier filing issues, and data mismatches before you file GSTR-3B.

What are GSTR-1 and GSTR-3B?

These are the GST returns that businesses actually file.

• GSTR-1 is used to report sales and outward supplies.

• GSTR-3B is the summary return used to report tax liability, claim ITC, and pay GST.

GSTR-2A and GSTR-2B sit between these two returns by helping businesses verify purchase data and available ITC before filing GSTR-3B.

Why is there no GSTR-2 return to file?

GSTR-2 was originally designed as a buyer-filed purchase return. However, it was suspended in 2017 because purchase information was already being captured through supplier filings and the matching process created significant complexity. Today, purchase data flows automatically into GSTR-2A and GSTR-2B based on supplier-reported invoices.

Rohan Sinha is a fintech and growth leader building aiaccountant.com, focused on simplifying accounting and compliance for Indian businesses through automation. An IIT BHU alumnus, he brings hands-on experience across 0 to 1 product building, growth, and strategy in B2B SaaS and fintech.