Key Takeaways

- Form 24Q is the quarterly TDS return for salary payments, filed under Section 192 of the Income Tax Act, 1961

- Every employer who deducts TDS from salary must file it, no turnover threshold, no exemptions based on company size

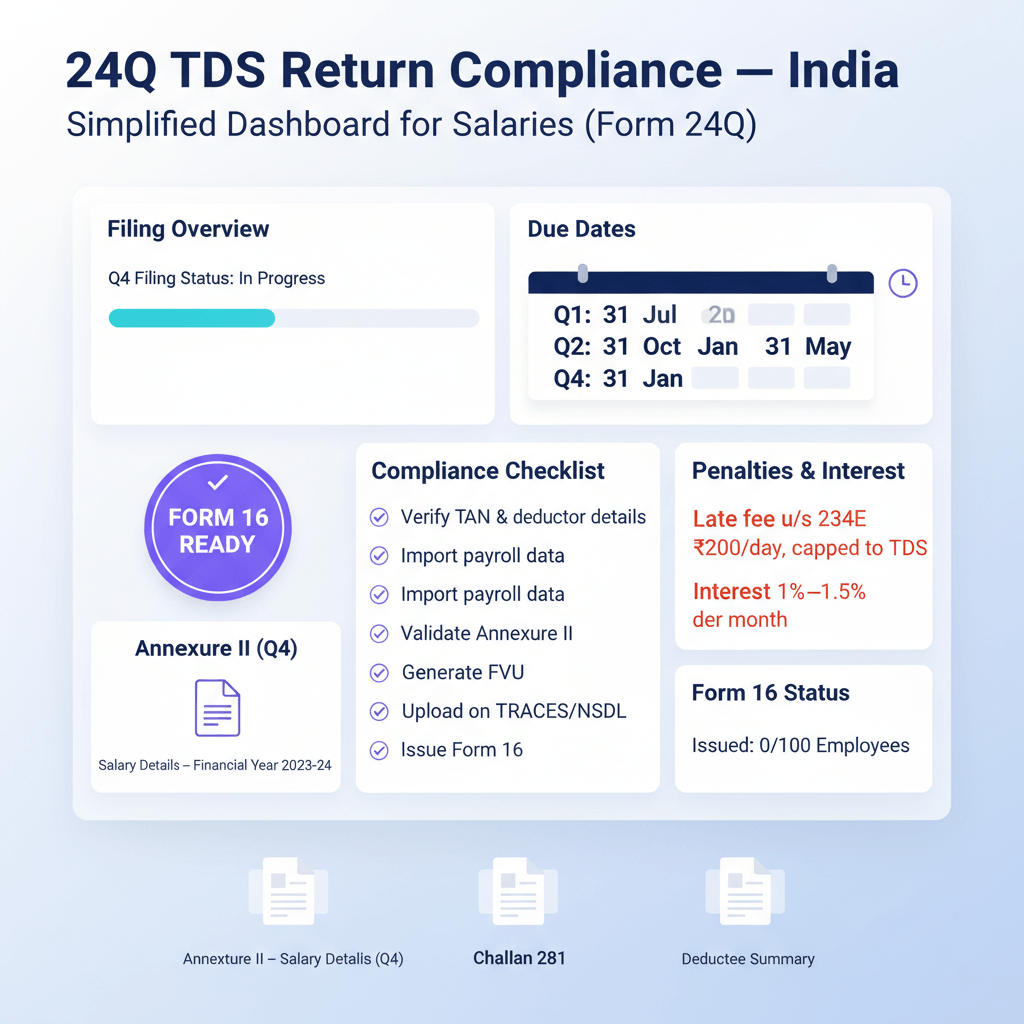

- Four quarterly due dates: Q1 → 31 July, Q2 → 31 October, Q3 → 31 January, Q4 → 31 May (not 31 March)

- The Q4 return is more complex, it includes Annexure II, a full year salary breakup for every employee

- Late filing attracts ₹200 per day under Section 234E, capped at the total TDS amount for that quarter, no waiver possible

- Form 16 must be issued by 15 June, but only after the Q4 Form 24Q is successfully filed and processed

- Missing even one quarter’s return is a compliance breach, all four must be filed independently

What Is Form 24Q: The Official Definition And Legal Basis

Form 24Q is the quarterly TDS return that every employer in India must file to report tax deducted at source from salary payments to employees. It is filed under Section 192 of the Income Tax Act, 1961, and submitted to the Income Tax Department four times a year, once for each quarter from April to March.

If you run a company in Bengaluru, a consulting firm in Delhi, or a D2C brand out of Mumbai, and you pay salaries, this return applies to you. The moment you deduct TDS from an employee’s salary, you are legally required to report it via Form 24Q, quarterly, not annually.

The return is also what makes your employees’ Form 16 possible. No properly filed 24Q means no valid Form 16. And no Form 16 means employees cannot accurately file their ITRs or claim TDS credit. The obligation is yours as the employer, not theirs.

If managing quarterly filings feels like a distraction from running your business, services like Virtual Accounting handle TDS end to end, but first, here is exactly what Form 24Q requires from you.

Form 24Q is the quarterly statement of tax deducted at source from salary, as defined under the Income Tax Act, 1961. The legal mandate sits in Rule 31A of the Income Tax Rules, 1962, which requires “every person responsible for paying salary” to furnish this statement quarterly.

The “person responsible” here is the employer, the deductor. Not the HR department, not the payroll vendor, not the employee. If you are signing salary cheques or approving payroll transfers, the compliance obligation is yours.

The purpose of Form 24Q is straightforward, it creates a central, verifiable record of every rupee of TDS deducted from salaries across India. The Income Tax Department uses this data to cross verify what your employees declare in their ITRs against what you actually deducted and deposited.

Once filed, the data flows to TRACES (TDS Reconciliation Analysis and Correction Enabling System) and shows up in each employee’s Form 26AS and Annual Information Statement (AIS). If your deduction is missing or wrong on TRACES, your employee’s ITR will have a mismatch, and that becomes your problem to fix.

Form 24Q is distinct from two other TDS returns you may have heard of:

- Form 26Q, for TDS on non salary payments, contractor fees, professional fees, rent, and more

- Form 27Q, for TDS on payments to non residents

Form 24Q is exclusively for salary. Section 192 only.

Who Must File Form 24Q: Employer Obligations And Thresholds

There is no minimum turnover threshold, no employee headcount cut off. The obligation is triggered by a single action, deducting TDS from salary.

If you are a private limited company in Pune with three salaried employees, you must file. If you are an LLP in Chennai, a partnership firm in Ahmedabad, or a proprietorship in Hyderabad that employs even one person whose salary crosses the basic exemption limit of ₹2.5 lakh per year, TDS kicks in under Section 192, and so does the Form 24Q obligation.

The full list of entities covered includes:

- Private and public limited companies

- LLPs and partnership firms

- Proprietorships and HUFs

- Trusts, societies, and NGOs that pay salaries

- Government deductors, central and state government departments

- Individuals acting as employers

Before you file even the first return, you must have a TAN (Tax Deduction Account Number), obtained via Form 49B. Filing without a TAN is not an option the system allows.

One nuance worth flagging, if you have a quarter with no salary payments you may file a nil return for the quarters with no payments. However, if you have never had any salaried employees, you may be exempt from filing nil returns, but once you have any deductee on record, quarterly filings are mandatory.

Government deductors follow the same return structure but use a Book Adjustment challan (Type “C”) instead of regular ITNS 281 challans. The filing obligation and deadlines are identical.

Inside Form 24Q: Structure, Annexures, And What You Actually Submit

Form 24Q is not a single flat form. It has two annexures, and which ones you submit depends on the quarter.

Annexure I: Filed For Q1, Q2, Q3, And Q4

Annexure I covers the basic mechanics of the TDS transaction. You are reporting:

- Deductor details: TAN, PAN, name, address, type of deductor

- Challan details: BSR code of the bank branch, challan serial number, date of deposit, total TDS deposited

- Deductee details, per employee: PAN, name, amount paid or credited, TDS deducted, surcharge, education cess, section code, always 192 for salary

Every quarter requires Annexure I. Think of it as the receipt level data, here is what you deducted, here is the challan proving you deposited it, here is which employee it relates to.

Annexure II: Filed Only With The Q4 Return

This is the one that makes Q4 significantly heavier than the other three quarters. Annexure II is a complete salary breakup for the entire financial year for each employee. It includes:

- Gross salary paid

- Allowances and exemptions claimed, HRA under Section 10(13A), LTA, and more

- Standard deduction under Section 16(ia), currently ₹50,000, revised to ₹75,000 from FY 2024-25 per Union Budget 2024

- Deductions under Chapter VI-A, Section 80C, max ₹1.5 lakh for instruments like PPF, ELSS, life insurance, Section 80D, health insurance, and others

- Net taxable income

- Total tax computed, tax deducted, and tax deposited

This is effectively the employer’s declaration of how they computed each employee’s tax liability for the year and how much TDS was deducted against it.

The Technical Filing Format

Returns are not filed as PDFs or Excel sheets. The process uses two free utilities from NSDL:

- RPU, Return Preparation Utility, a Java based tool where you enter all the data

- FVU, File Validation Utility, validates the prepared file for format errors and generates the .fvu file that is actually submitted

Submission is either via the TIN NSDL portal online or physically at a TIN FC, Tax Information Network Facilitation Centre. However, companies and government deductors whose total TDS in a year exceeds ₹1 lakh are required to file electronically only Form 24Q Electronic Filing Requirements.

Form 24Q Due Dates: Quarterly Filing Deadlines You Cannot Miss

This section is worth bookmarking. These are the two sets of deadlines that govern your salary TDS compliance.

TDS Deposit Deadline, Separate From Return Filing

TDS deducted from salary must reach the government account by the 7th of the following month. April TDS, deposited by 7 May. October TDS, deposited by 7 November.

The one exception, March TDS must be deposited by 30 April not 7 April. Government deductors must deposit the same day, or the next working day if using book adjustment.

Missing the deposit deadline triggers interest under Section 201(1A), covered in the next section.

24Q TDS Return Due Date: Quarterly Schedule

The 24Q TDS return due date is separate from the deposit deadline and follows this fixed schedule:

- Q1, 1 April to 30 June: 31 July

- Q2, 1 July to 30 September: 31 October

- Q3, 1 October to 31 December: 31 January

- Q4, 1 January to 31 March: 31 May

The Q4 due date, 31 May, catches employers off guard every year. Many assume it is 31 March because the financial year ends then. It is not. The Q4 deadline is extended to 31 May specifically because Annexure II requires compiling a full year of salary data for every employee. Build this into your compliance calendar from Day 1.

These are the standard statutory deadlines. CBDT occasionally issues circulars extending specific quarter deadlines, particularly in years with IT portal disruptions. Always verify the current year’s effective deadline on the CBDT website before assuming the standard dates apply.

One downstream deadline to note, Form 16 must be issued to employees by 15 June. This is only possible after the Q4 Form 24Q is filed by 31 May and processed on TRACES. Miss the 31 May return deadline and you will almost certainly miss the 15 June Form 16 deadline too, which creates a cascade of compliance issues for your employees during ITR filing season.

Penalties For Late Filing Or Non-Filing Of Form 24Q

This is not a regime where you can “pay the fine later and move on.” The penalties here stack, and some of them are automatic.

Section 234E: Late Filing Fee

₹200 per day for every day the return is not filed after the due date. The fee runs from the due date until you actually file. The only cap, the total fee cannot exceed the total TDS amount for that quarter. Section 234E

This is classified as a fee, not a penalty, which means no discretion, no waiver, no officer can choose not to levy it. It is auto calculated and auto levied.

A Q1 return with ₹80,000 in TDS, filed 60 days late, fee = ₹200 × 60 = ₹12,000. That is a straight cash cost for an administrative oversight.

Section 271H: Penalty For Failure To File Or Incorrect Filing

If the return is not filed within one year of the due date, or if it is filed with materially incorrect information, the Assessing Officer can impose a penalty of minimum ₹10,000 to maximum ₹1,00,000.

There is a safe harbour, no penalty under Section 271H applies if, TDS was deposited to the government, the Section 234E fee was paid, and the return was filed before expiry of one year from the due date. This is why filing late is always better than not filing at all.

Interest Under Section 201(1A)

Two rates, two scenarios:

- Late deduction, you deducted TDS later than required, 1% per month or part of month from the date tax was deductible to the date it was actually deducted

- Late deposit, you deducted but deposited late, 1.5% per month or part of month from the date of deduction to the date of actual deposit

A practical example, your Q1 TDS of ₹50,000 was deducted but deposited 3 months late. Interest = ₹50,000 × 1.5% × 3 = ₹2,250. That compounds across every quarter and every employee if the underlying process is broken.

How To File Form 24Q: Step By Step Process

- Deposit TDS Using Challan ITNS 281. Log in to the Income Tax portal and pay using net banking or authorised bank branches. Save the BSR code and challan serial number from the confirmation, you will need both when preparing the return.

- Download The RPU. Get the latest Return Preparation Utility from the NSDL TIN website. It is free and Java based. Use the latest version, older versions may not support recent schema changes.

- Prepare The Return. Enter deductor details, TAN, PAN, name, address, challan details from your ITNS 281 receipt, and deductee details, employee PAN, name, salary paid, TDS deducted. For Q4, complete Annexure II as well, gross salary, exemptions, deductions, final tax computation per employee.

- Validate Using FVU. Run the completed RPU file through the File Validation Utility, also from NSDL, also free. FVU checks for format and structural errors. If it passes, it outputs the .fvu file. If it fails, it gives you an error report, fix each error and re run.

- Submit The .fvu File. Upload on the TIN NSDL portal or carry it to a TIN FC if you are filing physically.

- Receive And Store The PRN. After submission, you get a Provisional Receipt Number, PRN. This is your proof of filing. Store it. You will need it if you ever file a correction return.

- Download Form 16 From TRACES. After Q4 Form 24Q is processed, log in to TRACES, download Form 16 Part A for each employee, and issue it to them by 15 June.

For businesses with larger payrolls or more complex salary structures, professionals typically use paid TDS software such as TDSMAN, Gen TDS, or Winman TDS instead of the free RPU. These tools handle bulk data, reduce manual errors, and integrate challan matching. If managing this end to end is pulling your finance team away from growth work, Virtual Accounting by AI Accountant handles TDS filings from ₹4,000 per month, learn more.

Common Mistakes In Form 24Q, And How To Avoid Them

Wrong or missing employee PAN. If a PAN is invalid or missing, TDS credit will not appear in the employee’s Form 26AS. Worse, under Section 206AA, TDS must be deducted at 20% if PAN is not available. Verify every PAN before filing, do not rely on what employees gave you at onboarding without checking it on the NSDL PAN verification tool.

Challan mismatch. A single wrong digit in the BSR code, challan date, or serial number means the TDS deposit does not reconcile with the return. Cross check every challan against the OLTAS ledger before finalising the return.

Wrong section code. Filing salary TDS under a non salary section, 194C, 194J, and others, means the data does not match the right head. Always use section code 192 for salary in Form 24Q.

Incomplete Annexure II in Q4. Not factoring in HRA exemption under Section 10(13A), ignoring LTA claims, or miscalculating 80C deductions leads to inflated TDS, employee complaints, and discrepancies in Form 16.

Filing only Q4 and skipping Q1 to Q3. Some employers think of TDS as an annual exercise. It is not. All four quarters are independent filings with independent deadlines and independent late fees. Q4 does not replace Q1 through Q3.

Not updating mid year joiners or leavers. An employee who joined in November must appear in Q3, not just Q4. An employee who resigned in July must have their details correctly captured in Q1 and Q2 only.

These are the errors that generate demand notices, block employee refunds, and create messy correction cycles.

How To Correct Or Revise A Filed Form 24Q

Mistakes in a submitted return are fixable. The correction process runs through TRACES, not the TIN NSDL portal.

TRACES supports several types of corrections, each with a code:

- C1, Update deductor details, name, address

- C2, Update challan details, BSR code, date, amount

- C3, Update deductee or salary details

- C4, Add a new challan

- C5, Update the PAN of a deductee

- C9, Add a new deductee row that was missed entirely

The correction workflow, log in to TRACES, request correction, select the quarter, choose correction type, download the Justification Report, it shows you exactly what the system flagged as errors, make corrections in RPU, re validate in FVU, upload the corrected .fvu file.

There is no statutory limit on the number of correction returns you can file. You can revise as many times as needed until the data is clean.

One practical requirement, you need the original PRN, Provisional Receipt Number from the initial filing to initiate any correction on TRACES. This is why storing PRNs from every quarter’s filing matters, treat them the way you treat GST acknowledgement numbers.

Corrections are not just a compliance formality. A wrong PAN or incorrect TDS amount in your 24Q means the employee’s Form 26AS shows the wrong credit. When they file their ITR, the system flags a mismatch, their refund gets delayed or rejected, and they escalate to you. Fix errors promptly, the legal and practical obligation to do so sits with the employer.

Wrapping Up: What You Need To Act On

File Form 24Q four times a year, 31 July, 31 October, 31 January, and 31 May. Deposit TDS by the 7th of every month, 30 April for March. File Annexure II with Q4. Issue Form 16 to every employee by 15 June.

Late filing costs ₹200 per day under Section 234E with no waiver possible. Non filing beyond one year risks a penalty of up to ₹1 lakh under Section 271H. Late deposit of TDS costs 1.5% per month in interest under Section 201(1A).

Your employees’ ITR filing, refund claims, and Form 26AS accuracy all depend on you getting this right. It is not paperwork for the government’s benefit, it is infrastructure for your team’s financial life.

If quarterly 24Q filings, challan reconciliation, Annexure II computation, and Form 16 issuance are pulling your team away from growth work, Virtual Accounting by AI Accountant handles TDS compliance end to end from ₹4,000 per month, get started.

FAQ

What Is The 24Q TDS Return Meaning In Simple Terms?

Form 24Q is the quarterly return filed by employers to report TDS deducted from employee salaries. It is submitted to the Income Tax Department under Section 192 of the Income Tax Act, 1961, four times a year, once per quarter.

Who Is Required To File Form 24Q?

Every employer who deducts TDS from salary, regardless of company size, turnover, or number of employees. This includes private limited companies, LLPs, partnership firms, proprietorships, HUFs, trusts, and government deductors.

What Is The 24Q TDS Return Due Date For Each Quarter?

Q1, April to June, 31 July. Q2, July to September, 31 October. Q3, October to December, 31 January. Q4, January to March, 31 May.

Why Is The Q4 Form 24Q Due Date 31 May And Not 31 March?

The Q4 return includes Annexure II, a complete salary breakup for the full financial year for every employee. This requires more time to compile accurately, so the deadline is 31 May.

What Is The Difference Between Annexure I And Annexure II In Form 24Q?

Annexure I contains challan details and deductee wise TDS breakup for the quarter, it is filed with all four quarters. Annexure II contains the full year salary computation including exemptions and deductions under Chapter VI A, it is filed only with the Q4 return.

What Happens If Form 24Q Is Not Filed On Time?

A late filing fee of ₹200 per day applies under Section 234E, from the due date until the actual date of filing, capped at the total TDS amount for that quarter. No waiver is available. Additionally, if the return is not filed within one year of the due date, a penalty of ₹10,000 to ₹1,00,000 can be imposed under Section 271H.

Can Form 24Q Be Filed If TDS Was Not Deducted In A Particular Quarter?

If you had salaried employees but their income was below the taxable threshold, a nil return can be filed. If you had no salaried employees at all in that quarter, filing requirements depend on whether you have any prior history of deductions under your TAN.

How Is Form 16 Connected To Form 24Q?

Form 16, Part A, is generated directly from the data in your filed Form 24Q. Specifically, Part A is downloaded from TRACES after the Q4 return is processed. If the Q4 Form 24Q is not filed by 31 May, Form 16 cannot be issued to employees by the 15 June deadline.

What Should I Do If I Made An Error In A Filed Form 24Q?

File a correction return through TRACES. Different correction types, C1 through C9, address different kinds of errors, challan details, PAN updates, salary figures, and more. You will need the original Provisional Receipt Number, PRN, from the initial filing to initiate the correction.

What Is The Penalty For Late Deposit Of TDS Deducted From Salaries?

Interest under Section 201(1A) applies at 1.5% per month, or part of month, calculated from the date of deduction to the date of actual deposit. For example, ₹50,000 deposited 3 months late incurs ₹2,250 in interest. This is separate from the late filing fee under Section 234E.