Key Takeaways

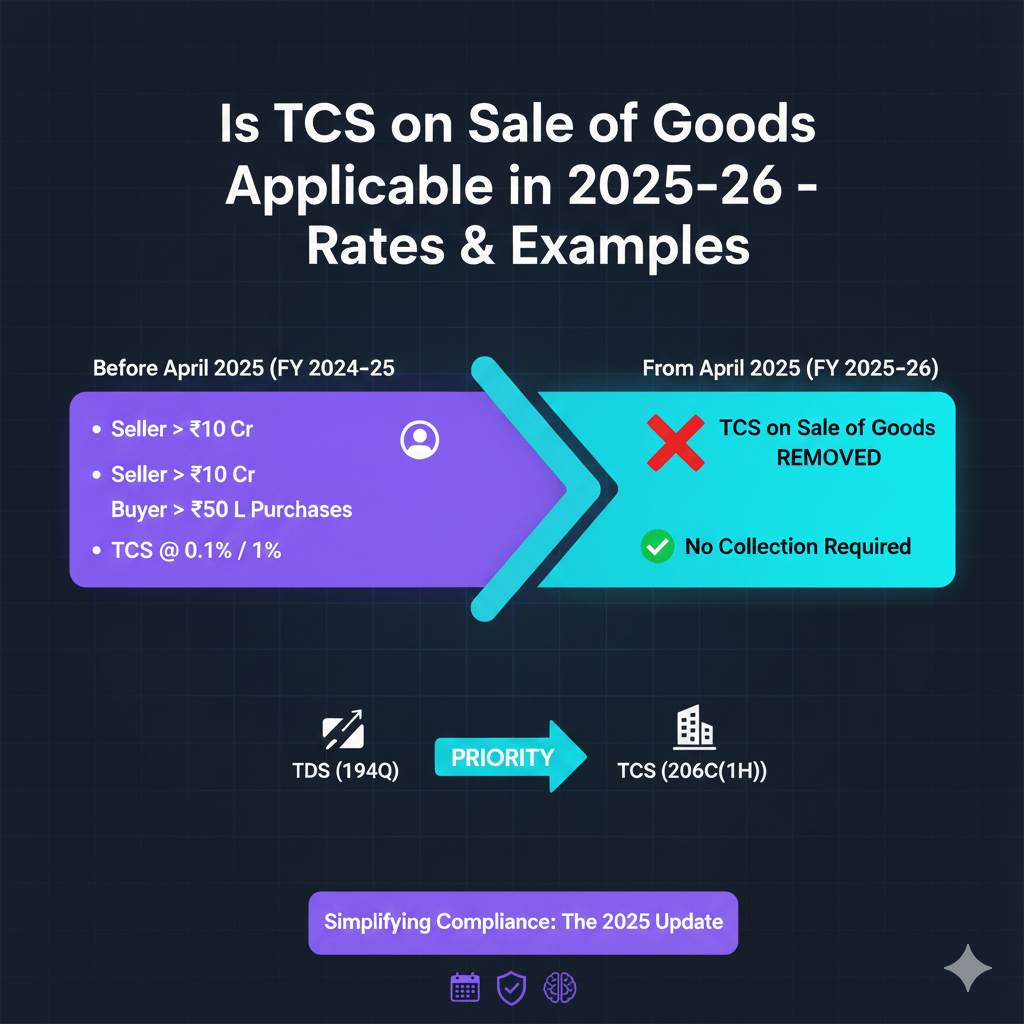

- TCS on sale of goods under Section 206C(1H) has been fully removed from 1 April 2025. Sellers no longer need to collect TCS on receipts exceeding ₹50 lakh from FY 2025–26 onwards.

- Until 31 March 2025, sellers with prior year turnover above ₹10 crore were required to collect TCS at 0.1% (or 1% without PAN/Aadhaar) on the portion of buyer receipts exceeding ₹50 lakh per financial year.

- The removal eliminates threshold monitoring, Form 27EQ filings, and Form 27D certificate issuance for this section, saving significant admin effort for finance teams and CA firms.

- Section 194Q (TDS on purchase of goods by buyers) remains unchanged. If your firm handles both buyer side and seller side compliance, only the seller side TCS workflow goes away.

- Businesses must still retain records for FY 2020–21 through FY 2024–25 to handle past audits, reconciliations, and closing obligations.

- Updating ERP and billing systems (like Tally) to disable the 206C(1H) TCS flag is a critical action item. Delays can lead to incorrect invoices or phantom TCS entries cluttering your books. Tools like AI Accountant's bookkeeping automation can help clean up legacy TCS entries and streamline the transition.

TCS on Sale of Goods Removed: What's New in 2026

If you're reading this in 2026, the good news is straightforward: Section 206C(1H) is history. But there are a few things worth flagging for this year specifically.

The year on year shift is complete. In FY 2024–25 (until 31 March 2025), sellers with turnover above ₹10 crore still had to track every buyer's cumulative receipts, flag the moment they crossed ₹50 lakh, and collect 0.1% TCS on the excess. From 1 April 2025 (FY 2025–26 onwards), that entire workflow is gone. No threshold tracking, no TCS collection, no Form 27EQ filing for this section. The Union Budget 2025 announcement via PIB confirmed this omission as part of broader TDS/TCS rationalization.

Who does the transition actually hit? Primarily mid to large sellers (₹10 crore+ turnover) in trading, manufacturing, and wholesale distribution sectors that dealt with hundreds of buyers crossing the ₹50 lakh mark. CA firms managing multiple such clients had the heaviest reconciliation load. For smaller businesses that were never covered, nothing changes operationally.

The real 2026 action items are about cleanup, not collection:

- Complete Q4 FY 2024–25 Form 27EQ filing if still pending (due date already passed; late filing attracts ₹200/day penalty under Section 234E).

- Reconcile TCS ledger balances in Tally or your ERP for FY 2024–25 before finalizing books. Any mismatch between TCS collected and TCS deposited will surface during assessment.

- Verify that your billing and accounting systems have disabled the 206C(1H) flag. Phantom TCS lines on invoices issued after April 2025 create unnecessary confusion for buyers and auditors alike.

- Retain all TCS records (Form 27D certificates, deposit challans, buyer threshold workings) for at least 6 to 8 years, since the assessment window under Section 149 can extend that far.

Section 194Q (TDS on purchase of goods) continues unchanged, so buyers with ₹10 crore+ turnover still need to deduct TDS at 0.1% when their purchases from a single seller cross ₹50 lakh. The removal of 206C(1H) doesn't affect this buyer side obligation. If you're managing both sides of the compliance for clients, platforms with automated reconciliation capabilities can help ensure nothing slips through during this transition period.

Cost of inaction: Failing to file pending Q4 FY 2024–25 TCS returns attracts a per day penalty. Unreconciled TCS deposits can trigger notices under Section 271H (penalty between ₹10,000 and ₹1,00,000). And if your system is still auto applying TCS on FY 2025–26 invoices, you're essentially collecting tax you have no authority to collect, which creates refund obligations and buyer disputes.

Tax Collected at Source (TCS) on the sale of goods was introduced under Section 206C(1H) of the Income Tax Act through the Finance Act 2020. It required certain sellers to collect a small percentage of tax from buyers once their annual purchases crossed a prescribed limit. The intent was simple: widen the reporting net and improve traceability of high value business transactions.

Ever since the provision came into force, the most common questions businesses have asked are: When is TCS applicable? Does it apply on all sales? What exactly is the ₹50 lakh threshold? And how do you calculate the amount correctly? These questions drive most search traffic today. Understanding them is essential for business owners, accountants, and finance teams, especially those searching for topics like "tcs on purchase of goods" and "section 206c of income tax act."

It's also important to note the major update in Budget 2025:

TCS on sale of goods under Section 206C(1H) has been removed starting FY 2025–26.

This makes it even more important to clearly understand how the rule worked until FY 2024–25, what changes from April 2025, and how businesses should manage the transition. If you've been searching for "is 206c 1h removed" or "section 206c(1h) removed," the answer is yes, it has been fully omitted.

In this article, we'll break down everything you need to know. That includes applicability conditions, turnover limits, the ₹50 lakh rule, TCS rates, calculation examples, exclusions, compliance requirements, and the latest 2025 amendments. All explained in a simple, practical way.

What Is TCS on Sale of Goods Under Section 206C(1H)?

TCS on the sale of goods means Tax Collected at Source according to Section 206C(1H) of the Income Tax Act. Laid down through the Finance Act 2020 and effective since 1 October 2020, this provision obliged selected sellers to collect a small percentage of tax from buyers once their purchases exceeded a certain limit. The regulation remained in force until its repeal from the financial year 2025–26 onwards.

According to this provision, a seller had to collect TCS from the amount paid by a buyer exceeding ₹50 lakh in a financial year if the seller's turnover in the previous year was more than ₹10 crore. Therefore, TCS on the sale of goods was a targeted compliance requirement. Only high value transactions and large businesses were concerned.

Who Was Responsible for TCS?

The responsibility lay entirely with the seller. Businesses with turnover above ₹10 crore were expected to collect TCS when they received payment from the buyer, deposit it with the government, and report it in their quarterly TCS return (Form 27EQ). Smaller businesses were not covered under this rule.

What Transactions Were Covered?

Section 206C(1H) applied strictly to the sale of goods, not services. It also excluded specific categories such as exports, imports, government purchases, and goods that were already taxed under other subsections (for example, motor vehicles under 206C(1F)).

In simple terms, if a buyer's annual purchases crossed ₹50 lakh and the seller met the turnover criteria, TCS became applicable on the excess amount.

TCS vs TDS — The Key Difference

While both are tax at source mechanisms, they operate differently.

- TDS is deducted by the buyer before making payment.

- TCS is collected by the seller at the time of receiving payment.

Another important rule was that if the buyer deducted TDS under Section 194Q, the seller did not have to collect TCS. TDS took priority. This is often referred to as the "priority rule" and was one of the most searched aspects of the TCS 206C interaction.

Applicability of TCS on Sale of Goods

TCS as per Section 206C(1H) was not meant to apply to all kinds of business or sales. It was applicable only if certain conditions were satisfied by the seller and the buyer.

Knowing these conditions was very important. Most misunderstandings about TCS had their origin in the question of whether a transaction was covered by this provision at all.

1. Seller's Turnover Threshold (₹10 Crore Rule)

The first condition was seller focused. TCS was to be charged only if the seller's total turnover in the last financial year was more than ₹10 crore. Small and mid sized business enterprises with a turnover below this limit were completely free from the TCS provisions of this section.

The turnover for this purpose was the revenue from all business activities of the seller, not just the goods covered by Section 206C(1H). Once the seller crossed the ₹10 crore threshold, they were required to keep track of the receipts from each buyer and collect TCS whenever it was due.

This is also the reason that queries like "tcs turnover limit", "10 crore tcs rule", and "tcs on sale of goods turnover limit" are very common. Many businesses wanted to find out if the rule applied to them.

2. Buyer Threshold (₹50 Lakh Rule)

The second provision considered the buyer's yearly purchase volume. TCS was required only when the total purchases of a buyer from a single seller crossed ₹50 lakh in a financial year.

TCS was not levied on the whole amount but only on that part which was above ₹50 lakh.

For example, if a buyer purchased goods worth ₹60 lakh, TCS was collected only on ₹10 lakh. This provision was a frequent source of confusion. Companies could not always ascertain if the threshold was to be applied to invoices, payments, or GST inclusive values.

The law clarified that TCS gets triggered upon receipt of the value exceeding the ₹50 lakh limit. GST is excluded when checking whether the threshold has been crossed, but the actual TCS amount is calculated on the receipt (which may include GST).

3. Nature of Transaction

Even if both monetary thresholds were met, TCS applied only to the sale of goods, not services. This distinction was important for businesses offering mixed supply (goods plus services), where only the goods component was considered for TCS calculation.

There were also several categories where TCS did not apply, including:

- Sales to the Central or State Government, local authorities, or embassies

- Export transactions

- Import of goods

- Goods already covered under other subsections such as 206C(1) (alcohol, tendu leaves, scrap, timber, certain minerals) and 206C(1F) (motor vehicles above ₹10 lakh)

Additionally, if the buyer deducted TDS under Section 194Q of the Income Tax Act, TCS was not applicable. TDS always took precedence.

TCS Rate on Sale of Goods

The TCS rate under Section 206C(1H) was relatively simple. After the buyers' total purchases in a year exceeded ₹50 lakh, the sellers had to collect TCS at 0.1% of the amount above ₹50 lakh. This rate was applicable when the buyer had given a valid PAN or Aadhaar and the payment was made towards the sale of goods.

When the buyer did not furnish PAN or Aadhaar, the TCS rate increased significantly to 1%. This is in accordance with Income Tax Act provisions which apply a higher rate for non compliant buyers. The large number of searches for phrases like "tcs rate on sale of goods" and "rate of tcs on sale of goods" reflects that many businesses failed to recognize this difference.

Another very important clarification: GST should not be considered while determining whether the ₹50 lakh limit has been crossed. The limit was for goods value only, not for the tax component.

However, when TCS was to be levied, the amount on which it was collected was the total receipt, which may have included GST. This is because the law required TCS to be collected at the time of "receipt" and not on the taxable value alone.

Practically, it implied:

- The value of goods was used to verify whether the threshold (₹50 lakh) had been crossed.

- The TCS amount (0.1% or 1%) was calculated on the payment received, which in most cases was inclusive of GST.

This twofold regulation was a common source of confusion among accountants and business owners.

How to Calculate TCS on Sale of Goods (With Examples)

Although the rule itself was simple, most confusion around TCS came from its calculation. This was especially true when buyers crossed the ₹50 lakh annual threshold through multiple transactions. The law required TCS to be collected only on the amount exceeding ₹50 lakh, and this applied on a per buyer, per year basis. Here's how the calculation works in real scenarios.

Example 1: Buyer Crosses the ₹50 Lakh Threshold

Suppose a buyer purchases goods worth ₹70 lakh from a seller during the financial year. The first ₹50 lakh is exempt under Section 206C(1H). TCS applies only to the excess ₹20 lakh.

At the standard TCS rate of 0.1%, the amount to be collected becomes:

TCS = ₹20,00,000 × 0.1% = ₹2,000

This example reflects the most searched scenario ("tcs above 50 lakhs with example") and shows that the rate applies only on the incremental amount.

Example 2: Buyer Crosses ₹50 Lakh Through Multiple Invoices

Many businesses hit the threshold gradually. Consider this situation:

- The first invoice of ₹30 lakh does not attract TCS, since the buyer hasn't crossed the limit yet.

- Later in the year, a second invoice of ₹25 lakh is raised. This pushes total purchases to ₹55 lakh.

Here, TCS applies only on the ₹5 lakh that exceeds the annual ₹50 lakh threshold, not on the full second invoice.

TCS at 0.1% becomes:

TCS = ₹5,00,000 × 0.1% = ₹500

This example highlights why companies needed ongoing tracking, not just invoice based calculations.

Example 3: When the Buyer Does Not Provide PAN or Aadhaar

If the buyer failed to provide a PAN or Aadhaar, the TCS rate increased dramatically to 1%, as per higher rate provisions under income tax rules.

Using the same figures as Example 1:

Amount above threshold = ₹20 lakh

Rate applicable = 1%

TCS collected = ₹20,00,000 × 1% = ₹20,000

The turnover and threshold logic remained the same. Only the rate changed because the buyer was considered non compliant.

Exclusions and Non-Applicability

Even in cases where a seller had a turnover of ₹10 crore or more and a buyer crossed the ₹50 lakh mark, TCS under Section 206C(1H) was not applicable to every transaction. There were quite a few exclusions in the provision. Most of the confusion around this rule resulted from the fact that people didn't know in which cases TCS was not required.

The first significant exclusion was export transactions. No TCS under this section was due on any sale of goods outside India, whether by direct export or deemed export. Correspondingly, imports were never covered since TCS is a collection instrument from a domestic buyer.

The other crucial restriction was that Section 206C(1H) referred to goods only and not services. Businesses in mixed supply (goods plus services) were required to apply TCS only on the goods component of the transaction.

TCS on Scrap Sale and Other Specific Goods

A common query relates to TCS on scrap sale. It's important to understand the distinction. Scrap was already covered under Section 206C(1), which has its own separate TCS provisions with different rates and conditions. Because scrap was already taxed under an existing subsection, it was specifically excluded from the scope of Section 206C(1H).

The same applied to other goods already covered under existing TCS provisions. These were:

- Goods under Section 206C(1) such as alcoholic liquor for human consumption, tendu leaves, timber, scrap, and certain minerals

- Motor vehicles covered under Section 206C(1F)

- Any transaction where TCS was already required under another subsection of 206C

Sales to specific entities were also exempt. The law excluded the Central and State Governments, local authorities, embassies, and other notified bodies from the definition of "buyer." As a result, TCS was not required on sales to these categories, regardless of transaction size.

A final and very critical exclusion involved the interaction with TDS under Section 194Q. If the buyer was liable to deduct TDS on the purchase of goods, then the seller was not required to collect TCS. TDS took clear priority over TCS, avoiding duplication and ensuring that only one form of tax withholding applied.

In summary, TCS under Section 206C(1H) applied only when all the core conditions aligned: seller eligibility, buyer threshold, and transaction type. The moment a transaction fell into any of the exclusions outlined above, TCS was not applicable.

TCS vs. TDS Under Section 194Q (Priority Rule)

One of the most important clarifications issued after the introduction of Section 206C(1H) was how it interacts with Section 194Q, the TDS provision on the purchase of goods introduced in July 2021. Many businesses faced uncertainty about whether both TDS and TCS applied, or which party was responsible for compliance.

The rule is actually straightforward:

If the buyer is required to deduct TDS under Section 194Q, then the seller does not collect TCS under Section 206C(1H).

In other words:

194Q overrides 206C(1H).

This "priority rule" ensures that only one tax at source mechanism applies to a single transaction. It also shifts the compliance burden based on who is eligible. TDS is buyer driven, while TCS is seller driven.

It's worth noting that while Section 206C(1H) has been removed from FY 2025–26 onwards, Section 194Q continues unchanged. Buyers with turnover exceeding ₹10 crore are still required to deduct TDS at 0.1% on purchases exceeding ₹50 lakh from a single seller. So the buyer side obligation on the purchase of goods remains fully active.

Comparison Chart: TDS (194Q) vs. TCS (206C(1H))

This simplified chart highlights the exact difference and the priority rule:

| Aspect | TDS under 194Q | TCS under 206C(1H) |

|---|---|---|

| Who is responsible? | Buyer deducts tax | Seller collects tax |

| Turnover condition | Buyer > ₹10 crore | Seller > ₹10 crore |

| Transaction threshold | Purchases > ₹50 lakh | Receipts > ₹50 lakh |

| Rate | 0.1% on amount above ₹50L | 0.1% (1% if no PAN) |

| When applied? | At time of credit/payment | At time of receipt |

| Priority rule | Overrides 206C(1H) | Applies only if 194Q does not |

| Status from FY 2025–26 | Continues unchanged | Removed |

| Outcome | TDS deducted → No TCS | TCS collected only when 194Q not applicable |

Latest Amendment – TCS on Sale of Goods Removed From FY 2025–26

Among major changes brought by the Budget 2025, the government announced a complete removal of TCS on the sale of goods under Section 206C(1H) from the next financial year. In other words, the provision, which had been operating since October 2020, is not applicable from 1 April 2025 anymore.

The decision to remove TCS from the sale of goods was a response to widespread critique. Businesses and tax experts pointed out that complying with TCS under Section 206C(1H) required constant buyer level tracking, receipt reconciliations, and monitoring of the ₹50 lakh limit. This made it difficult for sellers as well as accountants, especially in industries with large turnover.

For those searching for "tcs on sale of goods removed from april 1 2025 notification pdf," the official notification was part of the Finance Act 2025. The relevant clause omits Section 206C(1H) from the statute effective 1 April 2025. You can track the full text through the Income Tax Department portal.

Why the Government Removed TCS on Sale of Goods

The main reason is that the compliance load was too high compared to the revenue generated. For many businesses, the activity of monitoring whether a buyer had crossed the ₹50 lakh limit and collecting TCS at 0.1% caused more operational problems than the actual tax collected was worth.

The government recognized that the TCS rule had outlived its useful life. Other reporting modes such as TDS under Section 194Q and the increased transparency through GST data had made this provision redundant.

By removing the section, Budget 2025 aims to:

- Reduce repetitive reporting

- Eliminate double tracking of similar transactions

- Simplify compliance for midsize and large businesses

- Improve ease of doing business

TCS on Sale of Goods for FY 2025–26: Impact and Benefits

There are several immediate advantages of the elimination of TCS under Section 206C(1H):

- Sellers relief: Without the need to monitor buyer receipts, track thresholds, or collect and deposit TCS, sellers are relieved from a heavy administrative burden.

- Cash flow simplified: The additional outflow of 0.1% TCS that buyers used to face is no longer there. Sellers are also saved from reconciliation mismatches.

- Compliance simplified: Finance teams no longer need to prepare Form 27EQ, issue Form 27D certificates, or track monthly deposit timelines for this section.

- No more threshold tracking: The ₹50 lakh buyer limit, which was among the most frequent problems faced by ERPs and accounting systems, no longer needs to be monitored.

Transition: FY 2024–25 vs FY 2025–26

Companies should know the difference between two timeframes:

Until 31 March 2025:

The provisions of Section 206C(1H) remained in full force. Sellers who were required to collect TCS had to do so for all qualifying transactions during FY 2024–25. This includes filing Form 27EQ for Q4 and depositing any outstanding TCS amounts.

From 1 April 2025:

There is a complete removal of TCS on sale of goods. No collection is needed for FY 2025–26 onwards. Workflows already in place in ERP, accounting software (including Tally), and billing systems should be updated to reflect this change. Specifically, sellers should disable or set to zero any auto applied TCS percentage under 206C(1H).

For many companies, this transition simplifies year end processes, reduces monitoring requirements, and eliminates the need to deal with minor ledger differences caused by timing of receipts.

Businesses should also retain all TCS related records for FY 2020–21 through FY 2024–25. The assessment window under Section 149 of the Income Tax Act can extend to 6 to 8 years, so these records may be needed for future audits or notices.

Conclusion

TCS on the sale of goods under Section 206C(1H) was a fairly complex compliance requirement for businesses and accountants. While the provision caused more administrative work than anticipated, it also led companies to enhance their record keeping and reporting accuracy during the period it was applicable.

With the abolition of this section from FY 2025–26, the business community is relieved from the necessity to charge TCS on the sale of goods. However, knowing how the rule functioned is still vital for past filings, audits, and closing obligations until 31 March 2025.

Section 194Q (TDS on purchase of goods) continues unchanged, so buyer side compliance is still relevant. And for any historical queries around Section 206C of the Income Tax Act, this guide remains a comprehensive reference.

FAQ on TCS on Sale of Goods

1. Is TCS on sale of goods applicable in FY 2025–26?

No. TCS on sale of goods under Section 206C(1H) has been fully removed from 1 April 2025 (FY 2025–26 onward). Businesses no longer need to collect TCS on receipts above ₹50 lakh. TCS under this section was applicable only up to 31 March 2025. (2026 update)

2. Why was TCS on sale of goods removed?

The government withdrew the provision because the compliance burden was disproportionate to the tax revenue it generated. The rule duplicated oversight already available through TDS (Section 194Q) and GST data transparency. Budget 2025 removed it to simplify reporting for sellers and accountants.

3. Is Section 206C(1H) removed permanently?

Yes. Section 206C(1H) has been omitted from the Income Tax Act effective 1 April 2025 through the Finance Act 2025. This is a permanent legislative removal, not a temporary suspension. Other subsections of 206C (such as 206C(1) for scrap, timber, minerals and 206C(1F) for motor vehicles) continue to apply as before. (2026 update)

4. What was the TCS rate on sale of goods before it was removed?

The rate was 0.1% on receipts above ₹50 lakh per buyer per financial year, provided the buyer furnished PAN or Aadhaar. If PAN/Aadhaar was not provided, the rate was 1%. This is no longer charged after FY 2024–25.

5. Does TCS still apply on scrap sale after April 2025?

Yes, but under a different section. TCS on scrap sale falls under Section 206C(1), not 206C(1H). The removal of 206C(1H) does not affect TCS on scrap, timber, tendu leaves, minerals, or other goods covered under Section 206C(1). Those provisions remain fully active.

6. How did TCS interact with TDS under Section 194Q?

If TDS under Section 194Q applied, TCS under 206C(1H) did not apply. Section 194Q always had priority. This interaction no longer matters going forward since 206C(1H) is removed, but it remains relevant for assessments related to FY 2020–21 through FY 2024–25. Note that Section 194Q itself continues unchanged.

7. Do businesses need to update their ERP or billing systems?

Yes. From 1 April 2025, businesses should disable TCS calculation on receipts under 206C(1H), remove auto applied 0.1% charges, and stop threshold tracking against the ₹50 lakh rule. Sellers must also complete any pending Form 27EQ filing for Q4 FY 2024–25 and issue Form 27D certificates where required. After that, no further TCS on sale of goods applies under this section.